In the perfectly comepetive market structure, each firm is

a. A price maker

b. A price searcher

c. A price taker

d. A price fixer

C

Marginal revenue is

a. The change in revenue divided by price

b. The change in total revenue divided by total quantity sold

c. The change in total revenue for one additional unit sold

d. The change in sales priced per unit sold

C

In order to maximize profits, a firm should produce an output level for which

a. marginal revenue is equal to average cost

b. marginal revenue is equal to total cost

c. marginal revenue is equal to marginal cost

d. total revenue is equal to total cost

C

If a firm is producing an output level for which marginal revenue is less than marginal cost,

a. the firm can increase profits by producing and selling more output

b. the firm can increase profits by producing and selling less output

c. the firm is maximizing profits

d. whether or not the firm is maximizing profits cannot be determined

B

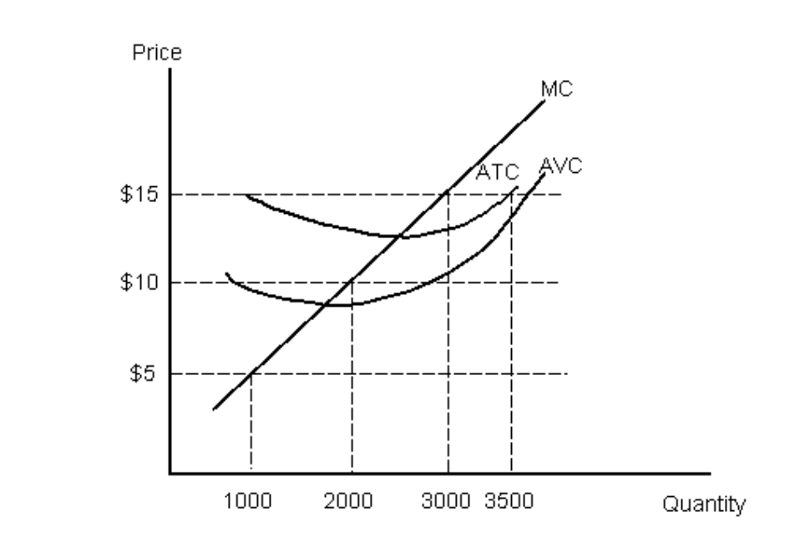

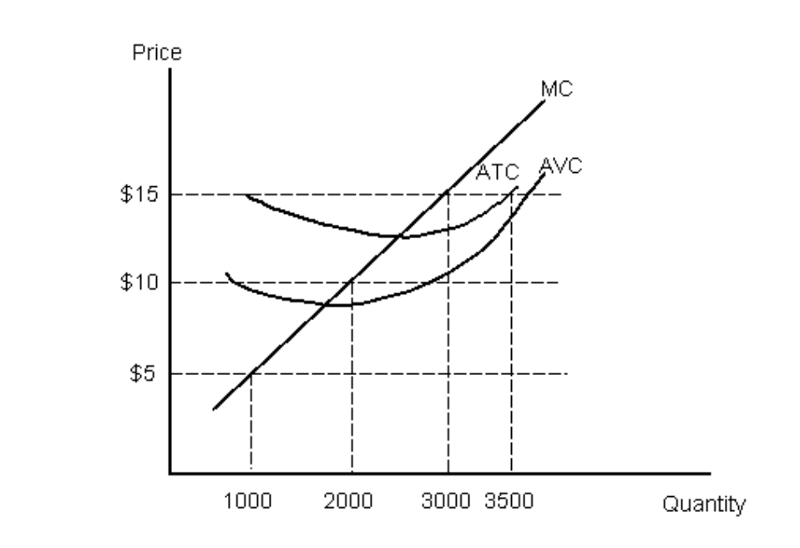

Figure A depicts the short-run marginal cost (MC), short-run average total cost (ATC) and short-run average variable cost (AVC) curves for a price-taking firm. If the market price is equal to $15, the profitmaximizing output level for the firm is ______________ and profits are ________________.

a. 3,500, positive

b. 3,000, positive

c. 3,000, negative

d. none of the above

B

Figure A depicts the short-run marginal cost (MC), short-run average total cost (ATC) and short-run average variable cost (AVC) curves for a price-taking firm. If the market price is equal to $10, the profit maximizing output level for the firm is ______________ and profits are ________________.

a. 3,500, positive

b. 3,000, negative

c. 2,000, negative

d. none of the above

C

The short-run supply curve for a price-taking firm is given by:

a. its entire short-run marginal cost curve

b. its short-run marginal cost curve above minimum average total cost

c. its short-run marginal cost curve above minimum average variable cost

d. the positively sloped portion of its average cost curve

e. its short-run marginal cost curve above average fixed cost

C

The industry/market supply curve is

a. Impossible to compute

b. The horizontal summation of the individual firm's supply curves

c. Is downward sloping

d. Is always equal to marginal product

B

Suppose you own a video rental store. Your monthly total revenue is $5,000. Your monthly variable costs are equal to $4,000. Additionally, you must pay $1,500 each month toward the lease of your store. In the short-run you should:

a. continue to operate, since profits are positive

b. continue to operate, despite negative profits

c. shut-down

d. none of the above

B

The perfectly competitive firm is a price:

a. maker

b. taker

c. searcher

d. fixer

B

A perfectly competitive firm produces and sells child car seats. The sales price is $600, the fixed costs are $3,000, and the variable costs are $300 per unit. What is the marginal revenue for the 10th seat sold?

a. $590

b. $625

c. $600

d. $480

C

In the VERY short run, _______________ is/are fixed and _______________ adjusts to clear the market.

a. price, quantity supplied

b. quantity supplied, price

c. both price and quantity supplied, demand

d. quantity demanded, quantity supplied

e. none of the above

B

In perfectly competitive markets, in the short-run,

a. the price of firms’ output is fixed

b. firms’ output levels are fixed

c. the number of firms operating in the market is fixed

d. all of the above

C

Everything else equal, in the short run, a rightward shift in demand will produce a larger increase in price relative to the resulting increase in quantity:

a. the more elastic is the supply curve

b. the more inelastic is the supply curve

B

Everything else equal, a rightward shift in supply will produce a larger decrease in price relative to the resulting increase in quantity:

a. the more elastic is the demand curve

b. the more inelastic is the demand curve

B

Which of the following conditions must hold in long-run equilibrium in perfectly competitive markets?

a. Firms earn zero economic profit

b. Price = Marginal Cost

c. Price = Average Total Cost

d. all of the above

D

In the long run, a shift in the demand curve to the left in a perfectly competitive market means:

a. the supply curve will shift to the right

b. price will increase and new firms will enter the market

c. price will decrease and firms will exit the market

d. quantity will not change

C

In a constant cost industry, the long-run supply curve is:

a. horizontal

b. upward sloping

c. downward sloping

d. undefined

A

Consider a perfectly competitive market in which firms have U-shaped long average costs which have a minimum of $20 at 100 units of output. The market is currently in long-run equilibrium, and a total of 20,000 units are produced and sold. What is the long-run equilibrium price in this market?

a. $2

b. $10

c. $15

d. none of the above

B

Consider the perfectly competitive market from the previous question in which firms have U-shaped long average costs which have a minimum of $20 at 100 units of output. The market is currently in long-run equilibrium, and a total of 20,000 units are produced and sold. How many firms are operating in this market?

a. 200

b. 300

c. 400

d. none of the above

A

In a perfectly competitive industry, the equilibrium price is $56 and the minimum average total cost of the industry's firms is $40. If this is a constant-cost industry, we would expect that in the long run:

a. new firms will enter the market, shifting the industry's short-run supply curve outward until the minimum average total cost rises to $56.

b. new firms will enter the market, shifting the industry's short-run supply curve outward until the new equilibrium price is $40.

c. new firms will enter the market, shifting the industry's short-run supply curve inward until firms are making positive profit.

d. existing firms will exit the market, shifting the industry's short-run supply curve inward until firms are breaking even.

B

For a monopolist,

a. marginal revenue is equal to price

b. marginal revenue is greater than price

c. marginal revenue is less than price

d. marginal revenue is undefined

C

For a single priced monopolist to increase sales it must

a. reduce the price of additional units sold

b. increase the price

c. decrease the price of all units

d. decrease the price if buyers want to purchase many units

C

Bubba Golf, a manufacturer of golf clubs, can sell 3 drivers at $600 each. To sell 4 drivers, Bubba Golf must lower the price to $580 each. The marginal revenue of the fourth club is:

a. $20

b. $60

c. $520

d. $580

C

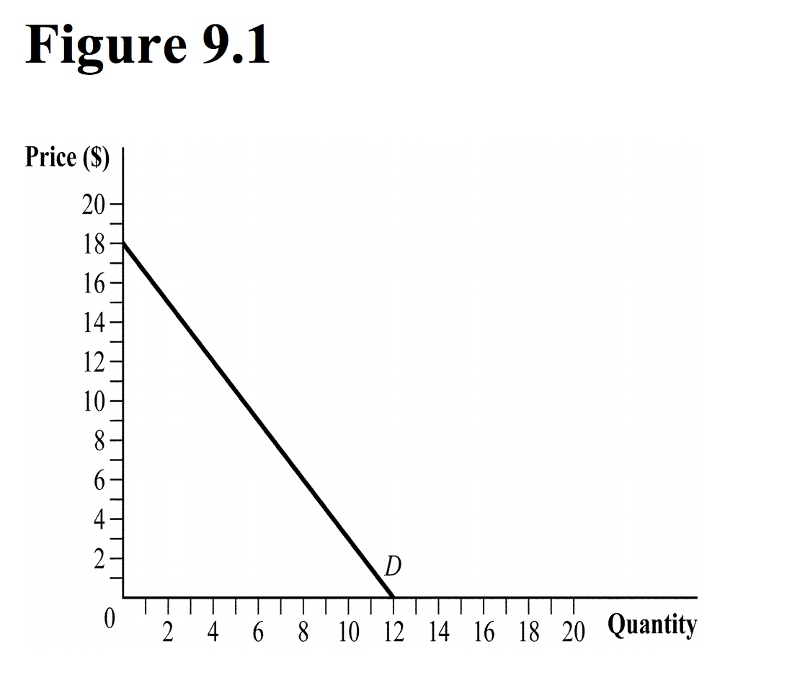

What is this firm's marginal revenue curve in Figure 9.1?

a. MR = 6

b. MR = 18 – 3Q

c. MR = 18 – 1.6Q

d. MR = 12 – 0.5Q

B

The single price monopolist sets price at

a. at the same point as a perfectly competitive firm

b. the point where demand equal marginal cost

c. the point where marginal cost equal average total cost

d. the point on the demand curve directly above the point where MC=MR

D

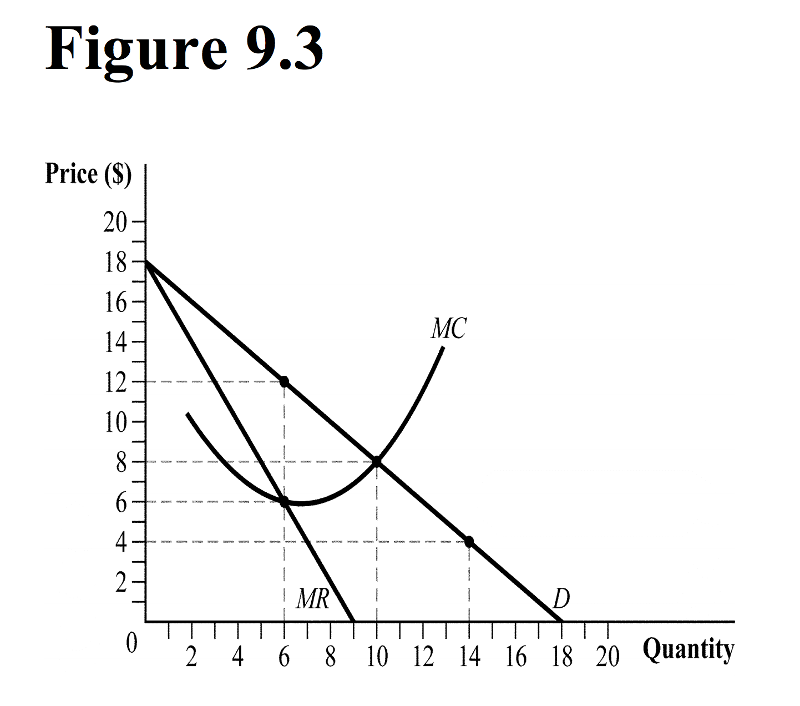

(Figure 9.3) The profit-maximizing quantity and price are ______ and ______, respectively.

a. 6 units; $6

b. 10 units; $8

c. 14 units; $4

d. 6 units; $12

D

A monopolist with constant average costs = 10 who faces a market demand given by Q=60 – P will produce _____ units of output and charge a price of _____.

a. 25; 10

b. 25; 35

c. 35; 25

d. 50; 10

B

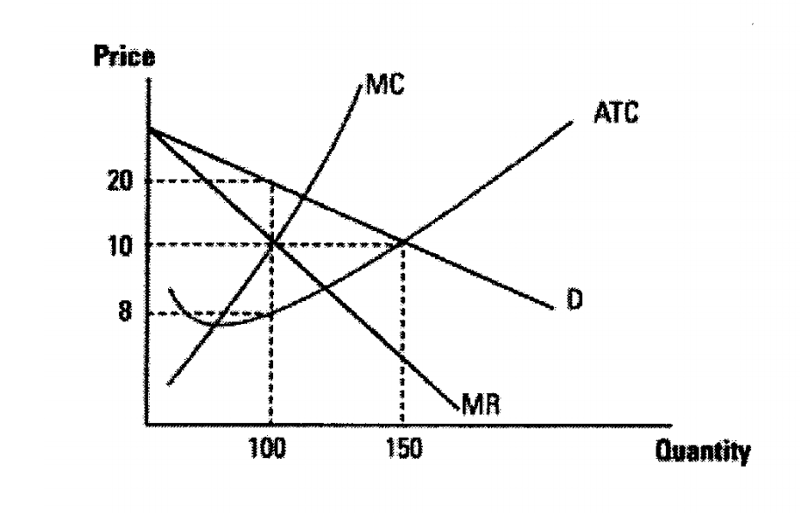

The diagram depicts the situation facing a monopolist. To maximize profits, the monopolist will produce _____________ units of output and charge a price of ___________. Profits to the firm are equal to _______________.

a. 100, $10, $200

b. 100, $20, $1200

c. 100, $20, $2000

d. 150, $10, $1500

B

A monopoly market is characterized by the inverse demand curve (which simply means is written as P = instead of the usual Q =): P = 1,200 – 40Q and a constant marginal cost of $200. If the marginal cost of production rises to $400, what happens to the profit-maximizing price and output level?

a. The profit-maximizing output level decreases by 6 units and the price rises by $100.

b. The profit-maximizing output level decreases by 2.5 units and the price rises by $100.

c. The profit-maximizing output level increases by 4 units and the price rises by $200.

d. The profit-maximizing output level decreases by 8 units and the price rises by $200.

B

The inverse demand curve for a monopolist changes from P = 100 – 2Q to P = 120 – 2Q, while the marginal cost of production remains unchanged at a constant $20. What happens to the profit-maximizing price and quantity following the change in the demand curve?

a. The price rises from $40 to $60, and the output rises from 20 units to 30 units.

b. The price rises from $60 to $70, and the output rises from 20 units to 25 units.

c. The price rises from $10 to $20, and the output rises from 100 units to 120 units.

d. The price rises from $50 to $60, and the output rises from 10 units to 12 units.

B

Unlike perfectly competitive firms, the monopolist:

a. has no well-defined supply curve

b. may earn positive economic profits in the long run

c. chooses both its output level and the price at which to sell it

d. all of the above

D

Compared to perfect competition, a monopolist charges a _____ price and sells _____ output.

a. higher; more

b. higher, less

c. lower, more

d. lower; less

B

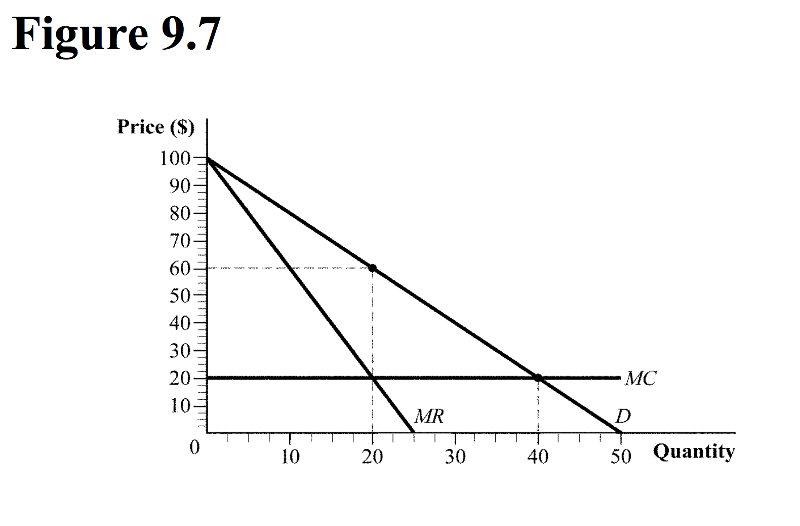

(Figure 9.7) The levels of consumer surplus under monopoly and perfect competition are ______ and ______, respectively.

a. $600; $2,000

b. $200; $400

c. $800; $3,200

d. $400; $1,600

D

(Figure 9.7) The levels of producer surplus under monopoly and perfect competition are ______ and ______, respectively.

a. $800; $0

b. $1,200; $0

c. $800; $400

d. $600; $200

A

If a monopolist is able to price discriminate via market separation, then it will maximize its profits by producing where ________________ in each market, and charging the group with the _______________ elastic demand a higher price.

a. P=MC, less

b. MR=MC, more

c. MR=MC, less

d. MR=AC, less

C

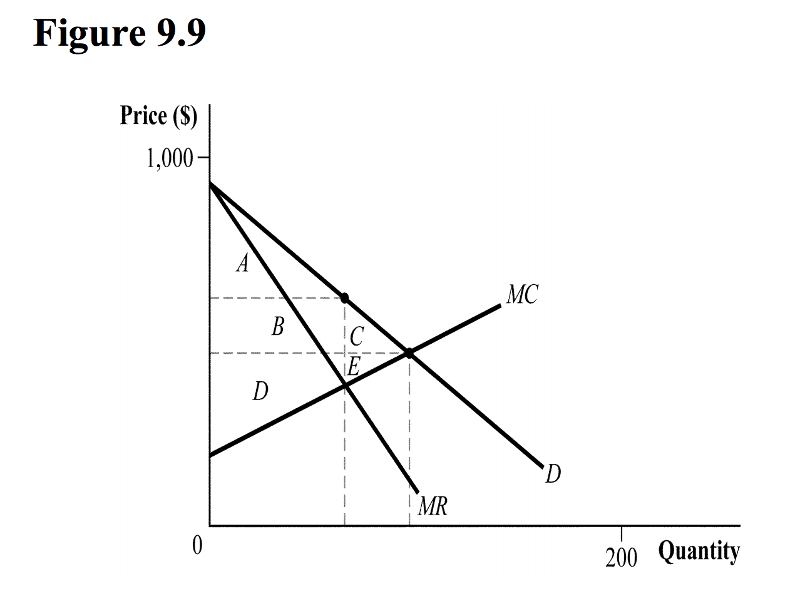

(Figure 9.9) Which of the following statements is TRUE?

I. Consumer surplus under perfect competition is given by area A + B + C.

II. Producer surplus under monopoly is given by area B + D.

III. The deadweight loss from market power is area C.

a. I, II, and III

b. I and II

c. III only

d. I only

B

The market called monopolistic competition is a market:

a. that produces homogeneous product

b. that produces a differentiated products

c. dominated by a large firm

d. in which firms act as price takers

B

Monopolistically competitive firms will produce at the point where:

a. MR=AVC

b. MR=MC

c. AFC=MC

d. MC=P

B

A monopolistic competitive market is one with:

a. a few interdependent firms

b. many small firms

c. several large firms

d. one large and many small firms

B

The demand curve in the monopolistic competitive market is a

a. vertical line

b. positively sloped line

c. negatively sloped line

d. horizontal line

C

A monopolistically competitive firm is like a perfectly competitive firm in that:

a. there are no barriers to entry

b. each firm produces an identical product

c. they have no market power (ability to set price)

d. all of the above

A

The monopolistically competitive graph looks just like the:

a. monopoly diagram

b. perfectly competitive diagram

c. monopoly diagram, but with a horizontal demand curve

d. perfectly competitive diagram, but with no supply curve

A

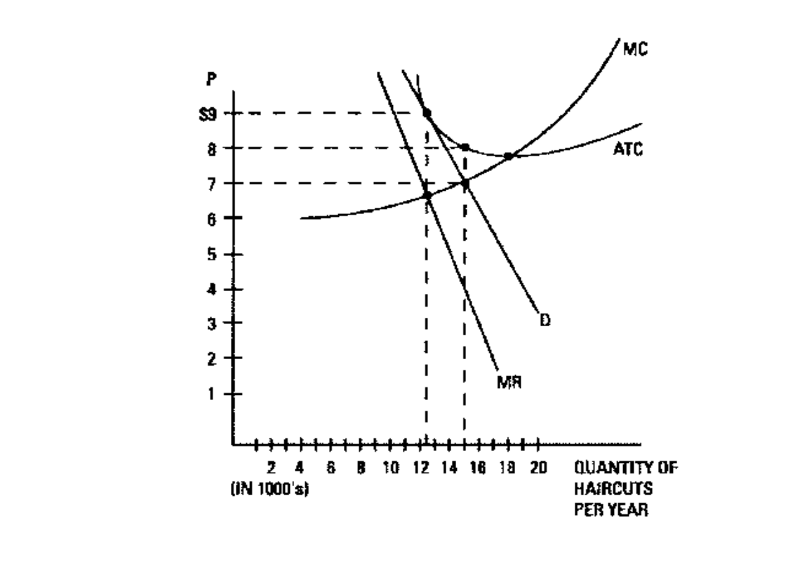

The figure depicts the situation for a typical barbershop in the monopolistically competitive market for haircuts. The firm will maximize profits by producing ________________ units of output and charging a price of ______________.

a. 15,000, $8

b. 15,000, $7

c. (approximately) 12,500, $9

d. (approximately) 12,500, (approximately) $6.50

C

The oligopoly market is comprised of

a. one firm

b. many small firms

c. companies selling services only

d. a few larger firms

D

The kinked demand model hypothesizes that each firm believes that other firms will:

a. not follow when it increases its price resulting in a more inelastic demand for higher prices

b. not follow when it increases its price resulting in a more elastic demand for higher prices

c. follow when it increases its price, resulting in a more inelastic demand for higher prices

d. follow when it increases its price, resulting in a more elastic demand for higher prices

B

The marginal revenue curve in the kinked demand model of oligopoly:

a. is a straight line with the same intercept as the market demand, but is twice as steep

b. has a segment that is horizontal

c. has a segment that is vertical

d. is equal to the market demand curve

C

In the simple classic Prisoner’s Dilemma game,

a. in equilibrium, one suspect confesses, the other does not

b. in equilibrium, both suspects do not confess

c. there are no dominant strategies

d. confessing is a dominant strategy

D