Firms may easily enter a monopolistically competitive market.

a.

True

b.

False

a. true

Product differentiation helps determine the slope of the demand curve facing a firm in monopolistic competition.

a.

True

b.

False

a. true

Monopolistic competitors are protected by barriers to entry.

a.

True

b.

False

b. false

The forces that determine the cost of production are largely independent of the forces that shape demand.

a.

True

b.

False

a. true

The term monopolistic competition

a.

is an alternate expression for monopoly

b.

is used to describe perfect competition with strong entry barriers

c.

denotes an industry with one seller of many differentiated products

d.

denotes an industry with many sellers of homogeneous products

e.

denotes an industry with many sellers of differentiated products

e. denotes an industry with many sellers of differentiated products

Monopolistically competitive industries consist of

a.

one firm selling several products

b.

one firm selling one product

c.

many firms, all selling identical products

d.

many firms, each selling a slightly different product

e.

many firms, each selling a completely different product

d. many firms, each selling a slightly different product

Collusion among firms to raise price is rare in monopolistically competitive markets because

a.

there are too many firms

b.

there are too few firms

c.

there is only one firm

d.

products are homogeneous

e.

price leadership is used instead

a. there are too many firms

Monopolistically competitive firms ignore the effect of their decisions upon other firms in the industry because

a.

each firm is large relative to the market

b.

each firm is small relative to the market

c.

there are few sellers in the market

d.

there is only one seller in the market

e.

all firms follow the same known pricing rules

b. each firm is small relative to the market

Monopolistic competition is different from perfect competition because monopolistic competitors produce

a.

a homogeneous product

b.

a homogeneous but unique product

c.

identical products

d.

differentiated products

e.

products similar to those produced by a monopoly

d. differentiated products

If Family Travel Agency, a monopolistic competitor, offers services that are differentiated from the services of other producers in the industry, it

a.

faces a perfectly elastic demand curve

b.

is a price taker

c.

has some power to control the price it charges

d.

faces a perfectly inelastic demand curve

e.

produces a product with no close substitutes

c. has some power to control the price it charges

A monopolistically competitive firm can raise price somewhat due to

a.

product differentiation

b.

barriers to entry

c.

product similarity

d.

its homogeneous product

e.

high tariffs

a. product differentiation

The demand curve facing Imelda's Shoe Boutique, a monopolistically competitive firm,

a.

is horizontal because Imelda's is small relative to the market as a whole

b.

is horizontal because Imelda's is large relative to the market as a whole

c.

slopes downward because Imelda's is small relative to the market as a whole

d.

slopes downward because Imelda's sells a differentiated product

e.

slopes downward because Imelda's firm is the entire industry

d. slopes downward because Imelda's sells a differentiated product

Monopolistically competitive firms use product differentiation to increase the price elasticity of demand.

a.

True

b.

False

b. false

Monopolistic competition is best described as

a.

many firms with some control over price, and some product differentiation

b.

many firms with no control over price, producing identical products

c.

a few firms with some control over price, producing highly differentiated products

d.

a few firms with no control over price, producing similar products

e.

a single firm producing all of the output for the industry, with strong control over price

a. many firms with some control over price, and some product differentiation

If a monopolistically competitive firm raises its price, it

a.

loses all of its customers (sales drop to zero)

b.

loses some, but not all, of its customers

c.

loses very few customers

d.

loses no customers at all

e.

gains customers (sales increase)

b.

loses some, but not all, of its customers

Which of the following is most likely produced in a monopolistically competitive market?

a.

soybeans

b.

autos

c.

fast food

d.

oil

e.

local phone service

c. fast food

Which of the following is most likely produced in a monopolistically competitive market?

a.

restaurant meals

b.

computer chips

c.

firewood

d.

motorcycles

e.

soft drink

a. restaurant meals

A firm could differentiate its product by all of the following means except one. Which is the exception?

a.

making the product available at a number of different locations

b.

increasing the number of services that accompany the product

c.

making the product physically different from other products

d.

using packaging or advertising to create a special subjective image of the product in the consumer's mind

e.

emphasizing that the product provides the same benefits to consumers as the others on the market, even when it is really physically different

e. emphasizing that the product provides the same benefits to consumers as the others on the market, even when it is really physically different

All of the following are examples of product differentiation except one. Which is the exception?

a.

developing a new video game or a computer program called "How to Teach Your New Dog Old Tricks"

b.

manufacturing a car that minimizes outside noise relative to other cars

c.

lowering the price of a good in a special sale

d.

providing movies and special meals on airline flights

e.

making sodium-free, caffeine-free colas

c. lowering the price of a good in a special sale

Economic analysis of product differentiation leads to all of the following conclusions except one. Which is the exception?

a.

Product differentiation makes it harder for firms to collude.

b.

Product differentiation makes price leadership harder to maintain.

c.

Product differentiation sometimes contributes to wasteful allocation of resources.

d.

Product differentiation must be based on real, substantive differences among products.

e.

There is a tradeoff between using resources efficiently and providing consumers with wide choices.

d. Product differentiation must be based on real, substantive differences among products.

When firms differentiate their products, they

a.

provide information to consumers with no additional use of productive resources

b.

always increase their profits

c.

always create real differences among products

d.

frequently create artificial or superficial differences among products, thus raising production costs

e.

usually strain the physical capacity of their plants

d. frequently create artificial or superficial differences among products, thus raising production costs

When firms in an industry produce differentiated products,

a.

long-run economic profit will always be zero

b.

short-run economic profit will always be positive

c.

the demand curves facing firms will always be perfectly elastic

d.

the demand curves facing firms will always be downward-sloping

e.

new firms will always have an incentive to enter the industry in the long run

d.

the demand curves facing firms will always be downward-sloping

Monopolistic competitors are

a.

price takers

b.

price searchers

c.

price maximizers

d.

price ignorers

e.

collusive price fixers

b. price searchers

In economics, products are considered "differentiated" only if

a.

they are physically or chemically different

b.

sellers decide that they are different

c.

buyers think that they are different

d.

the government determines that they are different

e.

they are produced by different firms

c. buyers think that they are different

Compared to regular grocery stores, convenience stores have

a.

higher prices and a more limited selection of goods

b.

higher prices and a greater selection of goods

c.

lower prices and a more limited selection of goods

d.

lower prices and a greater selection of goods

e.

equal prices and an equal selection of goods

a. higher prices and a more limited selection of goods

A monopolistically competitive firm produces where demand is inelastic.

a.

True

b.

False

b. false

Firms in monopoly or monopolistically competitive market structures do not have traditional supply curves as firms in perfect competition do.

a.

True

b.

False

a. true

A monopolistic competitor's demand curve is

a.

perfectly elastic

b.

less elastic than a monopolist's or oligopolist's but more elastic than a perfect competitor's

c.

as elastic as an oligopolist's

d.

more elastic than a monopolist's or oligopolist's but less elastic than a perfect competitor's

e.

perfectly inelastic

d. more elastic than a monopolist's or oligopolist's but less elastic than a perfect competitor's

The demand curve facing a firm will be more elastic,

a.

the fewer the number of competing firms

b.

the more differentiated the product

c.

the more substitutes there are for its product

d.

the greater the firm's ability to control price

e.

the larger the profit the firm can make

c. the more substitutes there are for its product

What do monopolistic competition, pure monopoly, and perfect competition have in common?

a.

free entry

b.

long-run economic profits

c.

differentiated product

d.

price taking

e.

the rule of profit maximization

e. the rule of profit maximization

In the short run, a monopolistically competitive firm is

a.

guaranteed to earn zero economic profit

b.

guaranteed to earn economic profit

c.

guaranteed to earn an economic loss

d.

guaranteed to earn either zero or positive economic profit

e.

not guaranteed any level of economic profit

e. not guaranteed any level of economic profit

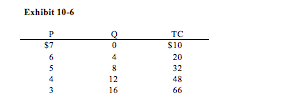

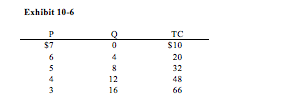

In Exhibit 10-6, what is the profit-maximizing price for this monopolistic competitor in the short run?

a.

$7

b.

$6

c.

$5

d.

$4

e.

$3

c. $5

In Exhibit 10-6, what is the maximum profit this monopolistic competitor can earn in the short run?

a.

$40

b.

$4

c.

$48

d.

$8

e.

$0

d. $8

If a monopolistically competitive firm can earn a profit, it will adjust production until

a.

MR > AVC

b.

MR = ATC

c.

MC > MR

d.

MR = AR

e.

MR = MC

e. MR = MC

Assume a monopolistically competitive firm is earning an economic profit. The marginal revenue from selling an additional unit is $30 and the marginal cost of producing that additional unit is $23. The firm should

a.

change neither its price nor its output level

b.

reduce its price and increase its output level

c.

increase its price and reduce its output level

d.

reduce both its price and its output level

e.

increase both its price and its output level

b. reduce its price and increase its output level

A rise in demand for restaurant meals is likely to cause which of the following in the short run?

a.

economic losses for each restaurant

b.

a lower price for each restaurant meal

c.

fewer restaurants in the industry

d.

more restaurants in the industry

e.

economic profit for restaurants

e. economic profit for restaurants

A rise in demand for restaurant meals is likely to cause which of the following in the long run?

a.

economic losses for each restaurant

b.

a lower price for each restaurant meal

c.

fewer restaurants in the industry

d.

more restaurants in the industry

e.

economic profit for restaurants

d. more restaurants in the industry

In both monopolistic competition and non-price-discriminating monopoly,

a.

the marginal revenue curve lies above the average revenue curve

b.

the marginal revenue curve lies above the demand curve

c.

the marginal revenue curve lies below the demand curve

d.

marginal revenue is equal to average revenue

e.

marginal revenue is equal to price

c. the marginal revenue curve lies below the demand curve

A monopolistically competitive firm is producing an output level at which marginal revenue is greater than marginal cost. This firm should __________ quantity and __________ price to increase profit or reduce losses.

a.

increase, increase

b.

increase; decrease

c.

decrease; increase

d.

decrease; decrease

e.

increase; not change

b. increase; decrease

A monopolistically competitive firm is producing an output level at which marginal revenue is less than marginal cost. This firm should __________ quantity and __________ price to increase profit or reduce losses.

a.

increase, increase

b.

increase; decrease

c.

decrease; increase

d.

decrease; decrease

e.

increase; not change

c. decrease; increase

Which of the following describes the relationship among market price (P), average revenue (AR), and marginal revenue (MR) for a firm in monopolistic competition.

a.

P = AR = MR

b.

P > AR = MR

c.

P = AR > MR

d.

P > AR > MR

e.

P = AR < MR

c. P = AR > MR

A profit-maximizing firm in monopolistic competition should shut down in the short run

a.

if marginal revenue is less than price

b.

if price is always less than average total cost

c.

if price is always less than average fixed cost

d.

if price is always less than average variable cost

e.

under no circumstances

d. if price is always less than average variable cost

In the long run in monopolistic competition, firms earn zero economic profit.

a.

True

b.

False

a. True

If a monopolistically competitive firm is in long-run equilibrium and average cost equals $150, then the market price must be $150.

a.

True

b.

False

a. true

Monopolistic competition is similar to

a.

perfect competition because the firms face downward-sloping demand curves and can earn only a normal profit in the long run

b.

pure monopoly because the firms face downward-sloping demand curves and can earn only a normal profit in the long run

c.

perfect competition because the firms face downward-sloping demand curves and similar to pure monopoly in that the firms can earn only a normal profit in the long run

d.

pure monopoly because the firms face downward-sloping demand curves and similar to perfect competition in that the firms can earn only a normal profit in the long run

e.

pure monopoly because the firms face downward-sloping demand curves and can earn an economic profit in the long run

d. pure monopoly because the firms face downward-sloping demand curves and similar to perfect competition in that the firms can earn only a normal profit in the long run

In the long run, a monopolistically competitive firm will

a.

produce a greater variety of goods than do firms in other market structures

b.

produce a greater output level than would a perfectly competitive firm

c.

produce where price equals average total cost

d.

earn an economic profit

e.

suffer a loss because of its advertising budget

c. produce where price equals average total cost

Suppose that a monopolistically competitive firm is in long-run equilibrium. The firm's demand curve is tangent to its average cost curve at Q = 25. Average cost is minimized at Q = 35, where average cost is $50. Which of the following is true?

a.

This firm maximizes profit at an output level of 25 units.

b.

This firm maximizes profit at an output level of 35 units.

c.

This firm maximizes profit at an output level less than 25 units.

d.

This firm maximizes profit at an output level greater than 35 units.

e.

There is not enough information to find the firm's profit-maximizing level of output.

a. This firm maximizes profit at an output level of 25 units.

Suppose that a monopolistically competitive firm is in long-run equilibrium. The firm's demand curve is tangent to its average cost curve at Q = 25. Average cost is minimized at Q = 35, where average cost is $50. Which of the following is true?

a.

This firm charges $50 for the good.

b.

This firm charges more than $50 for the good.

c.

This firm charges less than $50 for the good.

d.

The firm has excess capacity at all output levels greater than 35 units.

e.

Average cost is $50 at the profit-maximizing output level.

b. This firm charges more than $50 for the good.

Because of easy entry, monopolistically competitive firms will

a.

produce at the lowest average total cost

b.

charge a price equal to marginal cost

c.

earn no economic profit in the long run

d.

take advantage of all economies of scale

e.

earn no economic profit in the short run

c. earn no economic profit in the long run

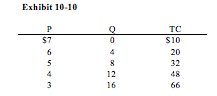

In Exhibit 10-10, what is the maximum profit this monopolistic competitor can earn in the long run?

a.

$40

b.

$4

c.

$48

d.

$8

e.

$0

e. $0

A firm will only earn normal profit in the long run

a.

if firms can freely enter or leave the market

b.

if firms do not try to maximize profit

c.

only if the industry is perfectly competitive

d.

whenever products are not differentiated

e.

if barriers to entry exist

a. if firms can freely enter or leave the market

In the long run, Bubba's Baby Boutique, a monopolistically competitive firm,

a.

earns zero normal profit but positive economic profit

b.

earns normal profit but zero economic profit

c.

earns normal and economic profit

d.

earns zero normal and economic profit

e.

might earn any level of economic profit; no level is guaranteed

b. earns normal profit but zero economic profit

In the long run, the economic profit of Hoot's Pump Chicken 'n' Ribs, a monopolistic competitor,

a.

is not eliminated because competition is not perfect

b.

is not eliminated because the demand curve slopes downward

c.

is eliminated because of new firms entering the industry

d.

is eliminated because of firms leaving the industry

e.

is not eliminated because new firms cannot enter the industryff

c. is eliminated because of new firms entering the industry

A permanent decrease in demand for convenience store services is likely to cause which of the following in the long run?

a.

an economic loss for each firm

b.

a higher price for each firm's output

c.

fewer firms in the industry

d.

more firms in the industry

e.

economic profit for each firm

c. fewer firms in the industry

If the firms in a monopolistically competitive industry are suffering short-run losses, which of the following will occur in the long run?

a.

Some firms will enter the industry.

b.

Customers of firms that leave the industry will switch to remaining firms.

c.

Firms that remain in the industry will face reduced demand.

d.

Firms will continue to incur losses.

e.

There will be no excess capacity.

b. Customers of firms that leave the industry will switch to remaining firms.

If the firms in a monopolistically competitive industry are earning short-run profit, which of the following is not likely to occur in the long run?

a.

New firms will enter the industry.

b.

New firms in the industry will draw customers away from existing firms.

c.

Existing firms in the industry will face a decrease in demand.

d.

Firms will continue to earn profit.

e.

Firms will produce with some excess capacity.

d. Firms will continue to earn profit.

In the long run in monopolistic competition, the demand curve facing the typical firm

a.

is perfectly elastic

b.

slopes upward

c.

is tangent to the firm's average total cost curve

d.

lies above the firm's average total cost curve

e.

is the same as the portion of the firm's marginal cost curve above average variable cost

c. is tangent to the firm's average total cost curve

As new monopolistically competitive firms enter the market, the demand facing each firm __________, causing the price charged by each firm to __________. In the long run, each firm will earn a __________ profit.

a.

falls; rise; positive

b.

rises; fall; positive

c.

falls; rise; normal

d.

rises; fall; normal

e.

falls; fall; normal

e. falls; fall; normal

If the demand curve facing the Acme Awl Company is tangent to its average total cost curve, all of the following statements are true except one. Which is the exception?

a.

Economic profit is zero.

b.

A normal profit exists.

c.

Marginal cost must exceed marginal revenue.

d.

Acme has excess capacity.

e.

Firms have no incentive to enter or leave this industry.

c. Marginal cost must exceed marginal revenue.

In the long run in monopolistic competition, a firm will not produce the output level that minimizes average cost because

a.

that output level is less than the profit-maximizing one

b.

at that output level, MC is greater than MR

c.

at that output level, P is greater than MR

d.

demand is horizontal

e.

that would leave the firm with excess capacity

b. at that output level, MC is greater than MR

Which of the following characteristics does perfect competition share with monopolistic competition?

a.

price-taking firms

b.

zero long-run economic profit

c.

homogeneous product

d.

some barriers to entry

e.

economies of scale in production

b. zero long-run economic profit

Monopolistically competitive firms

a.

are guaranteed to earn short-run economic profit

b.

may earn short-run economic profits, although long-run economic profit is typically zero

c.

may earn economic profit both in the short run and in the long run

d.

earn zero economic profit both in the short run and in the long run

e.

can only earn an economic profit in the inelastic portion of their demand curves

b. may earn short-run economic profits, although long-run economic profit is typically zero

In the long run, economic profit for a monopolistically competitive firm

a.

is zero, due to the lack of barriers to entry

b.

is zero, due to product differentiation

c.

may be positive, due to strong barriers to entry

d.

may be positive, due to product differentiation

e.

may be positive, due to advertising and product promotion

a. is zero, due to the lack of barriers to entry

In the long run, a monopolistically competitive firm will find

a.

its demand curve shifting until price equals average total cost

b.

its cost curve shifting until price equals average total cost

c.

its demand curve shifting until marginal revenue equals marginal cost

d.

its cost curve shifting until marginal revenue equals marginal cost

e.

no changes in its demand or cost curves if it is earning an economic profit

a.

its demand curve shifting until price equals average total cost

Suppose that firms in a monopolistically competitive industry are earning short-run economic profits. In the long run, the demand curve facing each individual firm can be expected to

a.

shift to the left and become flatter

b.

shift to the left and become steeper

c.

shift to the right and become flatter

d.

shift to the right and become steeper

e.

remain constant

a. shift to the left and become flatter

The first video rental outlets

a.

earned short-run economic profits because they faced little competition

b.

suffered short-run economic losses until videos caught on and demand for them increased

c.

were able to earn long-run economic profits because of barriers to entry

d.

earned only normal profits because the industry is perfectly competitive

e.

provided a good example of an oligopoly

a. earned short-run economic profits because they faced little competition

As a result of the economic profit earned by the first video rental outlets,

a.

existing firms were able to successfully lobby the government for patent protection

b.

competitors were attracted to the industry, and their entry reduced economic profit

c.

demand dried up

d.

Blockbuster saw an opportunity to take over the industry

e.

competitors were discouraged from entering the industry

b. competitors were attracted to the industry, and their entry reduced economic profit

The historical trend in the video rental industry

a.

has been one of increasing economic profits

b.

has been cyclical in the sense that profits decrease, then increase

c.

reflects the trend toward market concentration in all oligopolies

d.

has been one of increasing market concentration

e.

suggests the need for government regulation to eliminate price discrimination

d. has been one of increasing market concentration

Fixed costs in the video rental industry are

a.

high because of the extensive advertising in that industry

b.

high because of economies of scale

c.

low because of economies of scale

d.

higher in the long run than in the short run

e.

low

e. low

In the long run in monopolistic competition, all economies of scale are exhausted.

a.

True

b.

False

b. false

Excess capacity is defined as the difference between a firm's maximum possible output and its actual output.

a.

True

b.

False

b. false

Which of the following is inconsistent with the model of perfect competition?

a.

ease of entry into an industry

b.

ease of exit from an industry

c.

many buyers and sellers in the industry

d.

advertising of product differences in the industry

e.

a horizontal demand curve facing each firm in the industry

d. advertising of product differences in the industry

In which of the following market structures is a firm most likely to advertise extensively and fear entry of new firms?

a.

perfect competition

b.

pure monopoly

c.

monopolistic competition

d.

oligopoly

e.

both perfect competition and monopolistic competition

c. monopolistic competition

Which of the following is true of the relationship between price and marginal cost under monopolistic competition?

a.

P = MC at all levels of output

b.

P = MC only at the profit-maximizing quantity

c.

P > MC at the profit-maximizing quantity

d.

P < MC at the profit-maximizing quantity

e.

P < MC at the quantities below the profit-maximizing quantity

c. P > MC at the profit-maximizing quantity

In long-run equilibrium, a monopolistically competitive firm will produce

a.

at the minimum average cost

b.

at full capacity

c.

along the downward-sloping portion of its ATC curve

d.

along the upward-sloping portion of its ATC curve

e.

at the minimum of marginal cost

c. along the downward-sloping portion of its ATC curve

At the profit-maximizing output, price is greater than marginal cost

a.

for a monopolistically competitive firm only in the short run

b.

for a monopolistically competitive firm only in the long run

c.

for a monopolistically competitive firm in both the short run and the long run

d.

for a perfectly competitive firm only in the short run

e.

for a perfectly competitive firm only in the long run

c. for a monopolistically competitive firm in both the short run and the long run

In the long run, the output of a monopolistically competitive firm

a.

exceeds that of an otherwise similar perfectly competitive firm

b.

is less than that of an otherwise similar perfectly competitive firm

c.

is at the point at which LRAC is minimized

d.

equals that of an otherwise similar perfectly competitive firm

e.

is less than that of an otherwise similar monopolist

b.

is less than that of an otherwise similar perfectly

competitive firm

A monopolistically competitive firm

a.

earns no long-run economic profit and is therefore allocatively efficient

b.

earns no long-run economic profit and therefore produces at the minimum point of its ATC curve

c.

earns no long-run economic profit and is allocatively efficient even though it is not producing at the minimum point of its ATC curve

d.

earns no long-run economic profit, is allocatively inefficient, and does not produce at the minimum point of its ATC curve

e.

has a chance of making a long-run economic profit and is therefore allocatively inefficient

d. earns no long-run economic profit, is allocatively inefficient, and does not produce at the minimum point of its ATC curve

Although both perfectly competitive and monopolistically competitive firms earn normal profits in the long run, monopolistically competitive firms will not

a.

operate where price equals marginal cost

b.

charge a higher price than firms in perfect competition

c.

produce a smaller quantity than firms in perfect competition

d.

produce where price equals average total cost

e.

exit when demand falls below long-run average costs

a. operate where price equals marginal cost

Which of the following is true of firms in both monopolistic competition and perfect competition?

a.

Firms face a horizontal demand curve.

b.

Price exceeds marginal revenue.

c.

Firms can enter and leave the industry with relative ease.

d.

Price exceeds marginal cost.

e.

Products are differentiated.

c.

Firms can enter and leave the industry with relative ease.

One difference between perfect competition and monopolistic competition is that

a.

in perfect competition, firms cannot earn a long-run economic profit

b.

in perfect competition, firms take full advantage of economies of scale in long-run equilibrium; in monopolistic competition, firms do not

c.

only under perfect competition is there ease of entry and exit

d.

in monopolistic competition, the firm's demand curve is horizontal; in perfect competition, the firm's demand curve slopes downward

e.

in perfect competition, there are many firms; under monopolistic competition, there are few firms

b. in perfect competition, firms take full advantage of economies of scale in long-run equilibrium; in monopolistic competition, firms do not

Which of the following characteristics does perfect competition have in common with monopolistic competition?

a.

price-taking firms

b.

homogeneous products

c.

no barriers to entry

d.

horizontal demand curve

e.

neither market advertises

c. no barriers to entry

Compared to a firm in perfect competition, the monopolistically competitive firm tends to

a.

produce less and charge a higher price

b.

produce less and charge a lower price

c.

produce more and charge a lower price

d.

produce more and charge a higher price

e.

produce the same quantity

a. produce less and charge a higher price

Excess capacity typically occurs

a.

in the short run in perfect competition

b.

in the short run in monopolistic competition

c.

in long-run equilibrium in perfect competition

d.

in long-run equilibrium in monopolistic competition

e.

usually in markets experiencing an increase in demand

d. in long-run equilibrium in monopolistic competition

Which of the following is unique to perfect competition?

a.

The individual firm cannot earn economic profit in the long run.

b.

It is easy for new firms to enter the industry.

c.

The market demand curve slopes downward.

d.

The demand curve facing an individual firm is perfectly elastic.

e.

The firms in the industry produce a homogeneous product.

d.

The demand curve facing an individual firm is perfectly elastic.

Monopolistically competitive firms do not achieve allocative efficiency in the long run because

a.

marginal cost equals marginal revenue

b.

marginal cost is greater than marginal revenue

c.

marginal cost is less than marginal revenue

d.

price is less than marginal cost

e.

price is greater than marginal cost

e.

price is greater than marginal cost

Monopolistically competitive firms do not achieve productive efficiency because

a.

entry of firms raises production costs in the long run

b.

barriers to entry allow profit to be earned in the long run

c.

price is greater than marginal cost at the profit maximizing output level

d.

profit is maximized at a quantity where average total cost is not minimized

e.

there is no threat of entry in the long run

d.

profit is maximized at a quantity where average total cost is

not minimized

Firms in monopolistic competition and perfect competition typically

a.

are price takers

b.

produce identical products

c.

earn zero economic profit in the long run

d.

face a downward-sloping demand curve

e.

face an upward-sloping total revenue curve at all rates of output

c.

earn zero economic profit in the long run

Monopolistic competition is similar to

a.

perfect competition, in that firms face downward-sloping demand curves and earn zero long-run economic profit

b.

pure monopoly, in that firms face downward-sloping demand curves and can earn economic profits both in the short run and in the long run

c.

perfect competition, in that firms face perfectly elastic demand curves and earn zero long-run economic profit

d.

pure monopoly, in that firms can earn economic profits both in the short run and in the long run, and similar to perfect competition, in that firms face perfectly elastic demand curves

e.

pure monopoly, in that firms face downward-sloping demand curves, and similar to perfect competition, in that long-run economic profit is zero

e.

pure monopoly, in that firms face downward-sloping demand

curves, and similar to perfect competition, in that long-run economic

profit is zero

f marginal revenue is less than price for a firm, it must be true that the firm

a.

is a monopoly

b.

is in perfect competition

c.

is in monopolistic competition

d.

faces a perfectly elastic demand curve

e.

faces a downward-sloping demand curve

e.

faces a downward-sloping demand curve

Which of the following characteristics distinguishes oligopoly from other market structures?

a.

a horizontal demand curve

b.

a downward-sloping demand curve

c.

production of homogeneous outputs

d.

production of differentiated outputs

e.

interdependence among firms in the industry

e.

interdependence among firms in the industry

Oligopolistic industries consist of

a.

a few independent firms

b.

a few interdependent firms

c.

many interdependent firms

d.

many independent firms

e.

a small monopoly

b.

a few interdependent firms

The automobile, breakfast cereal, and tobacco industries are examples of

a.

monopolistic competition

b.

oligopoly

c.

perfect competition

d.

monopoly

e.

monopsony

b. oligopoly

The defining characteristic of oligopoly is that each firm

a.

produces the same output as its rivals

b.

acts independently of its rivals

c.

is mutually interdependent

d.

is atomistic

e.

advertises how its products are different from its rivals' products

c. is mutually interdependent

An intersection known as Four Corners lies 300 miles from the nearest town. At this intersection are three independently owned gas stations and one small pharmacy. Which of the following is true?

a.

The firms are all perfectly competitive because of their size.

b.

It would be easier for all four firms to form a cartel than for only the gas stations to do so.

c.

The gas stations are monopolistically competitive because there are so few of them that they are almost monopolists.

d.

The gas stations are perfectly competitive; the pharmacy is not.

e.

The gas stations are oligopolists; the pharmacy is a monopolist.

e.

The gas stations are oligopolists; the pharmacy is a monopolist.

Which of the following is unique to oligopoly among all the market structures?

a.

product differentiation

b.

profit maximization

c.

mutual interdependence

d.

advertising

e.

long-run economic profits

c.

mutual interdependence

Oligopolists are more sensitive to the pricing and output policies of their rivals when

a.

all firms produce identical products

b.

their products are highly differentiated

c.

there is freedom of entry and exit

d.

there are barriers to entry

e.

there are many firms in the industry

a.

all firms produce identical products

The defining characteristic of oligopoly is product differentiation.

a.

True

b.

False

b. false

Something is called a barrier to entry only if it makes entry into an industry absolutely impossible.

a.

True

b.

False

b. false

When there are barriers to entry, a profit-maximizing firm already in the industry can charge any price it wants, even in the long run.

a.

True

b.

False

b. false

It is harder to explain the behavior of firms in oligopoly than in other market structures because in oligopoly

a.

the firms act independently of each other

b.

firms base their decisions on what their rivals do

c.

only differentiated products are produced

d.

only homogeneous products are produced

e.

the demand curve can slope upward

b.

firms base their decisions on what their rivals do

Which of the following is not considered a barrier to entry?

a.

economies of scale

b.

patents

c.

control of a scarce resource

d.

licensing

e.

perfect price discrimination

e.

perfect price discrimination

For firms in an oligopoly to be interdependent,

a.

goods must be undifferentiated

b.

goods must be differentiated

c.

firms must be small

d.

barriers to entry must be minimal

e.

goods can be either undifferentiated or differentiated

e.

goods can be either undifferentiated or differentiated

An oligopoly is characterized by

a.

few firms, which have control over market price

b.

many firms and some barriers to entry

c.

a large number of firms and no barriers to entry

d.

a single firm and no barriers to entry

e.

a single firm and significant barriers to entry

a.few firms, which have control over market price

In which market structure(s) might firms produce an undifferentiated product?

a.

perfect competition only

b.

perfect competition and oligopoly

c.

monopolistic competition only

d.

perfect competition and monopolistic competition

e.

monopoly only

b.

perfect competition and oligopoly

If Ford raises the price of its automobiles, the demand curve for GM automobiles

a.

shifts to the left

b.

is unaffected

c.

becomes more elastic

d.

shifts to the right

e.

becomes vertical

d.

shifts to the right

In an oligopoly, the demand curve facing an individual firm depends upon

a.

the behavior of competing firms

b.

the shape of the firm's average total cost curve

c.

the shape of the firm's marginal cost curve

d.

the firm's supply curve

e.

the shape of the firm's average variable cost curve

a.

the behavior of competing firms

Interdependent decision making on price, quality, or advertising is characteristic of

a.

perfect competition

b.

monopolies

c.

oligopolies

d.

monopolistic competition

e.

both oligopolies and monopolistic competition

c.

oligopolies

There are multiple models of pricing behavior in oligopolistic markets because

a.

it is difficult to predict how rival firms will react to any pricing decision

b.

the demand curve slopes upward for these firms

c.

firms could earn profit in the long run unlike other markets

d.

price has a direct impact on profit for a firm in oligopoly

e.

the products are not identical in terms of quality, image, location

a.

it is difficult to predict how rival firms will react to any

pricing decision

In oligopoly, minimum efficient scale is large relative to the market.

a.

True

b.

False

a. true

Economies of scale yield

a.

declining average cost as output increases

b.

declining marginal cost as output increases

c.

declining total cost as output increases

d.

diminishing average returns as output increases

e.

increasing marginal revenue as output increases

a.

declining average cost as output increases

The automobile industry is

a.

in monopolistic competition because brand names are important

b.

in monopolistic competition because it has economies of scale

c.

in monopolistic competition for legal reasons

d.

an oligopoly because each firm must produce a large amount of output before it can achieve low average costs

e.

an oligopoly for legal reasons

d.

an oligopoly because each firm must produce a large amount of

output before it can achieve low average costs

If a firm must produce a significant share of market output before low average costs can be achieved, the structure of this industry will tend to be

a.

monopolistic competition

b.

perfect competition

c.

oligopoly

d.

either monopolistic competition or oligopoly

e.

either perfect competition or monopolistic competition

c.

oligopoly

Which of the following is not an example of an oligopolistic barrier to entry?

a.

diseconomies of scale

b.

legal restrictions

c.

advertising and brand proliferation

d.

high start-up costs

e.

control over an essential resource

a.

diseconomies of scale

Oligopolists often sacrifice economies of scale as they expand product variety.

a.

True

b.

False

a. True

A brand name may contribute to oligopolists' economic profit by

a.

shifting the demand curve leftward

b.

shifting the supply curve leftward

c.

overcoming economies of scale

d.

acting as a barrier to entry

e.

reducing advertising costs

d.

acting as a barrier to entry

The various models of oligopoly explain observed behavior in different industries, but none is satisfactory as a general theory of oligopoly.

a.

True

b.

False

a. true

Which of the following is an example of an actual cartel?

a.

the three largest cereal producers in the United States

b.

General Motors, Ford, and Chrysler

c.

the Organization of Petroleum Exporting Countries (OPEC)

d.

the three major U.S. cigarette manufacturers

e.

U.S. television networks -- ABC, NBC, CBS, and Fox

c.

the Organization of Petroleum Exporting Countries (OPEC)

Collusion is most likely to occur in those oligopolies in which firms have vastly different cost structures.

a.

True

b.

False

b. false

Collusion and cartels are frequently legal in Europe.

a.

True

b.

False

a. true

An oligopolist that cheats on a collusive agreement by reducing price will quickly be forced out of the industry by its competitors.

a.

True

b.

False

b. false

The incentives for oligopolists to cheat on collusive agreements are strongest during periods of increasing industry sales.

a.

True

b.

False

b. false

Collusion occurs when

a.

a firm chooses a level of output to maximize its own profit

b.

firms get together to maximize joint profits

c.

firms refuse to follow their price leaders

d.

firms petition their U.S. senators for favors

e.

two firms' price and output decisions come into conflict

b.

firms get together to maximize joint profits

If all six suppliers of cement to Metropolis all agree to establishes a price of $45 per ton, this would be

a.

a legal contract

b.

price discrimination

c.

cost-plus pricing

d.

a cartel

e.

beneficial to consumers

d.

a cartel

Collusion is easier to achieve and maintain in oligopoly when

a.

there are many firms in the industry

b.

the firms' products are homogeneous

c.

the firms' cost structures are very different

d.

there are very weak barriers to entry

e.

the industry is located in the United States

b. the firms' products are homogeneous

Which of the following does not hinder successful price leadership?

a.

all of the following are correct

b.

potentially large economic profits due to this activity

c.

cheating by offering secret discounts

d.

product differentiation

e.

illegality of coordinated pricing

b.

potentially large economic profits due to this activity

Historically, the U.S. steel industry has been a good example of

a.

monopolistic competition

b.

a cartel

c.

a pure monopoly

d.

the kinked demand curve model of oligopoly

e.

the price leadership model of oligopoly

e.

the price leadership model of oligopoly

During certain periods in the past few decades, if one of the three major breakfast cereal producers in the United States announced a price increase, the other two announced a similar price increase. This is a good example of

a.

monopolistic competition

b.

a cartel

c.

a pure monopoly

d.

the kinked demand curve model of oligopoly

e.

the price leadership model of oligopoly

e.

the price leadership model of oligopoly

Cost-plus pricing

a.

is used only in oligopolistic market structures

b.

simplifies pricing policy by adding a markup to average total cost

c.

in actual practice leads to markups which are greater for more elastic demand curves

d.

is likely to increase profits more than the use of marginal analysis

e.

requires the firm to project the amount which will be sold and then "mark-up" the price based on average variable cost

e.

requires the firm to project the amount which will be sold

and then "mark-up" the price based on average variable cost

Price wars occur more often in monopolistic competition than in other market structures.

a.

True

b.

False

b. false

A payoff matrix is a table listing the expected economic profit resulting from different possible strategies.

a.

True

b.

False

a. true

In the game theory model of oligopoly,

a.

firms will be successful in colluding to raise prices

b.

one firm raises its prices, and other firms follow suit

c.

firms will match other firms' price cuts but not their price increases

d.

firms may attempt to avoid the worst outcome but may achieve a less-than-optimal outcome

e.

firms never avoid the worst outcome

d.

firms may attempt to avoid the worst outcome but may achieve

a less-than-optimal outcome

In game theory, if two rivals in an oligopoly can avoid a large loss by cutting price from $40 to $35,

a.

neither will cut its price

b.

one will charge $40 and the other will charge $35

c.

their actions will depend on their respective strategies

d.

each will cut price but not all the way to $35

e.

they will collude to do what's best for both of them

c.

their actions will depend on their respective strategies

One common assumption in game theory is that firms

a.

try to avoid the worst outcome

b.

try to achieve the best outcome

c.

minimize losses

d.

always cooperate

e.

always compete

a.

try to avoid the worst outcome

Game theory is a separate model of oligopoly therefore it is of limited value when trying to generally understand firm level behavior

a.

True

b.

False

b. false

Game theory provides us with a general approach to understanding the behavior of firms when their choices are interdependent

a.

True

b.

False

a. true

The prisoner's dilemma is applicable only when considering the illegal behavior that firms in a non-competitive market may pursue

a.

True

b.

False

b. false

A player's strategy is a game plan when decisions are interdependent

a.

True

b.

False

a. true

Because firms in an oligopoly are interdependent, they attempt to maximize revenues rather than profits

a.

True

b.

False

b. false

Game theory is most useful in understanding the decision making behavior of firms in which type of industry?

a.

perfect competition

b.

monopoly

c.

monopolistic competition

d.

natural monopoly

e.

oligopoly

e. oligopoly

Game theory focuses on

a.

strategic behavior among interdependent firms

b.

professional athletic events

c.

competition between the players in board games

d.

competition between those in the political arena and those in the market place

e.

the interaction between firms in a competitive industry and those in a non-competitive industry

a.

strategic behavior among interdependent firms

Game theory is used in a number of areas in economics. What is the primary reason that it is used in analyzing oligopoly type market structures?

a.

The firms are producing a similar product

b.

The firms are producing differentiated products

c.

The demand curve facing the oligopolistic firms is perfectly inelastic

d.

The mutual interdependence of firms in industries with a small number of firms

e.

The demand curve the oligopolistic firm faces is downward sloping

d.

The mutual interdependence of firms in industries with a

small number of firms

Game theory is the study of which of the following?

a.

The prisoner's dilemma

b.

The behavior of people engaged in recreational games

c.

The mutual interdependence of firms in oligopolistic industries

d.

The downward sloping demand curve faced by firms in an oligopoly

e.

The interaction between marginal and average revenue

c.

The mutual interdependence of firms in oligopolistic industries

The solution of a game is dependent upon

a.

predicted response of competitors

b.

the existence of a perfectly inelastic demand curve

c.

costs of production being constant

d.

economies of scale in production

e.

marginal revenue being equal to marginal cost

a.

predicted response of competitors

Which of the following is likely to occur when it is known that a two-person game is to be played only once?

a.

Collusion

b.

The demand curve becomes perfectly inelastic for this time period

c.

The prisoner's dilemma

d.

The pursuit of profit maximization for the entire industry

e.

An attempt to equate marginal revenue with marginal cost

b.

The demand curve becomes perfectly inelastic for this time period

A prisoner's dilemma is a situation in which

a.

a change in marginal cost may not lead to a change in price

b.

a firm's competitors follow a price increase but ignore a price decrease

c.

oligopolists behave irrationally

d.

oligopolists attempt to maximize sales rather than profits

e.

an oligopolists demand curve may become perfectly inelastic

a.

a change in marginal cost may not lead to a change in price

Which of the following is likely to occur when a two-person game can be played repeatedly?

a.

Collusion and cooperation among the players

b.

The prisoner's dilemma

c.

The industry demand curve will become perfectly elastic

d.

The industry demand curve will become perfectly inelastic

e.

There is no solution possible because of the indeterminate price quantity combinations

a.

Collusion and cooperation among the players

A prisoner's dilemma can be described as a situation in which

a.

a decision maker is uncertain about the potential punishment for something done in the past

b.

an individual decision maker finds it in his best interest to pursue a course of action that can lead to a less than desirable outcome for the group

c.

producers act so as to avoid maximizing profits because of government retaliation

d.

individual firms seeks to maximize their own profits with no regard for the group

e.

the summation of individual demand curves creates an inelastic demand curve facing the industry

b.

an individual decision maker finds it in his best interest to

pursue a course of action that can lead to a less than desirable

outcome for the group

The principal advantage of the game theory approach is that it allows us to

a.

take all possible information into consideration before developing a theory

b.

better understand why the firm in a competitive industry avoids games

c.

better understand how the government should regulate a natural monopoly

d.

better understand decision making when one person’s choices affect another person’s choices

e.

understand the relationship between the firm and the industry demand curves

d.

better understand decision making when one person’s choices

affect another person’s choices

The advantage of game theory is that it allows us to focus on the

a.

individual firm's incentives to cooperate or not

b.

relationship between the market and firm level demand curve

c.

costs and benefits

d.

government regulators and the firms in an industry

e.

models where there are no barriers to entry

a.

individual firm's incentives to cooperate or not

The term strategy in terms of game theory refers to

a.

the relationship between price and marginal cost

b.

the relationship between individual firm demand curves and the market demand curve

c.

each firm's game plan in making decisions

d.

the interrelationship between price and marginal revenue

e.

the tendency for collusive firms to generate normal profits

c.

each firm's game plan in making decisions

The payoff matrix refers to

a.

the difference between total revenue and total cost at different price levels

b.

a listing of the rewards and penalties associated with pursuing various strategies

c.

the difference between average and marginal cost for the non-competitive firm

d.

the difference between average and marginal revenue in a non-competitive industry

e.

the difference between average variable and average total cost to the firm

b.

a listing of the rewards and penalties associated with

pursuing various strategies

The solution in the prisoner's dilemma is called the

a.

loss minimizing solution

b.

profit maximizing equilibrium

c.

dominant-strategy equilibrium

d.

revenue maximizing equilibrium

e.

marginal revenue solution

c.

dominant-strategy equilibrium

The dominant-strategy solution implies that each firm

a.

ignores the reactions of competitors

b.

colludes with competitors to maximize industry profits

c.

ignores the decisions of the other firms

d.

takes all potential bits of information into consideration before making a decision

e.

selects the optimal solution to a game

c.

ignores the decisions of the other firms

The prisoner's dilemma provides an explanation for

a.

the price wars that sometimes occur in oligopolies

b.

the ability of firms in an oligopoly to extract the entire consumer surplus

c.

the collusive behavior that sometimes occurs in an oligopoly

d.

the failure of firms in non-competitive industries to maximize profits

e.

an irrational behavior that occurs in competitive markets

a.

the price wars that sometimes occur in oligopolies

The tit-for-tat strategy implies that the firms

a.

in non-competitive industries match price increases but ignore price decreases

b.

will follow the lead of the dominant firm in making pricing decisions

c.

prices will change whenever fixed cost changes

d.

cooperate on the first round, and then follow your competitors reactions on the second round

e.

price will only change if demand changes

d.

cooperate on the first round, and then follow your

competitors reactions on the second round

Which oligopoly model was developed to explain price wars in an industry?

a.

natural oligopolies

b.

cartels

c.

price leadership by a dominant firm

d.

game theory

e.

cost-plus theory

e.

cost-plus theory

In a game that can be repeated, the optimal solution is

a.

dependent upon each firm's decision in the first round of decision making

b.

independent of the decisions that competitive firms made on the first round

c.

to maximize profits regardless of what competitors do

d.

to minimize costs regardless of what competitors do

e.

to select the solution that minimizes the potential losses from a decision

a.

dependent upon each firm's decision in the first round of

decision making

As a real estate agent, Krista Otavi prides herself on her good training, availability to clients, and hard work to make a sale. Which one of the basic ways of product differentiation does Krista emphasize?

a.

services

b.

product image

c.

location

d.

commission rate

e.

physical differences

a.

services

A greater supply of video rental outlets along with the increased availability of substitutes like cable channels made rental rates

a.

decrease slightly

b.

remain unchanged

c.

crash

d.

fluctuate wildly up and down

e.

increase

c.

crash

Which of the following is not a threat to bricks-and-mortar video rental stores?

a.

on-demand movies delivered by broadband cable

b.

rental services that deliver DVDs by mail

c.

digital movies and TV shows available on Wal-Mart’s Web site

d.

None of the answers is a threat.

e.

All of the answers are threats.

e.

All of the answers are threats.

In regards to monopolistic competition, some economists argue that consumers are willing to pay a higher price in order to enjoy a wider selection of goods and services.

a.

True

b.

False

a. true

If the leading canned soup company introduces dozens of new flavors in order to dominate shelf space, the company is most likely trying to create a barrier to entry by

a.

increasing the total investment needed to reach the minimum efficient size

b.

spending more on advertising than potential competitors can afford

c.

exploiting economies of scale

d.

crowding out the competition

e.

establishing an undifferentiated oligopoly

d.

crowding out the competition

To maximize cartel profit, the members must allocate output so that the marginal cost for the final unit produced by each firm is

a.

identical

b.

unequal

c.

negative

d.

equal to the firm’s average total cost

e.

maximized

a.

identical

Consensus becomes easier to achieve as the number of firms in a cartel grows

a.

True

b.

False

b. false

In the prisoner’s dilemma game, the sentence that each player receives depends on

a.

neither strategy chosen

b.

only the strategy the player chooses

c.

only the strategy the other player chooses

d.

the strategy the player chooses and on the strategy the other player chooses

e.

None of the answers is correct.

d.

the strategy the player chooses and on the strategy the other

player chooses

In a coordination game, a Nash equilibrium occurs when

a.

each player ignores the strategy of the other player

b.

each player chooses no strategy, but maintains the status quo

c.

each player chooses the same strategy

d.

one player can improve the outcome by changing strategy

e.

None of the answers is correct.

c.

each player chooses the same strategy

If oligopolists engaged in some sort of collusion, industry output would be __________ and the price would be __________ than under perfect competition.

a.

smaller, lower

b.

smaller, higher

c.

smaller, no different

d.

greater, lower

e.

greater, higher

b. smaller, higher

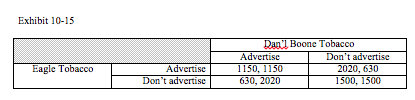

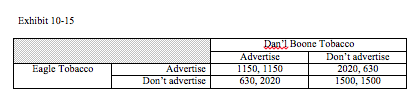

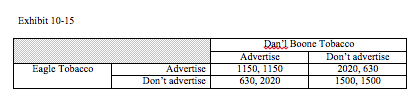

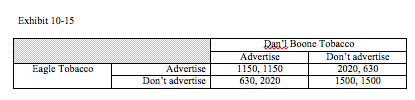

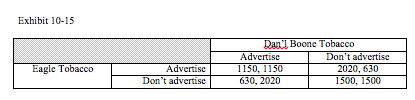

Exhibit 10-15 depicts the payoff matrix facing Eagle Tobacco and Dan’l Boone Tobacco with respect to their decisions to advertise or not. What strategies will maximize their joint profit?

a.

Eagle advertise and Dan’l Boone doesn’t

b.

both advertise

c.

Eagle doesn’t advertise and Dan’l Boone does

d.

neither advertises

e.

can’t tell

d.

neither advertises

Exhibit 10-15 depicts the payoff matrix facing Eagle Tobacco and Dan’l Boone Tobacco with respect to their decisions to advertise or not. What strategies will most likely result?

a.

Eagle advertise and Dan’l Boone doesn’t

b.

both advertise

c.

Eagle doesn’t advertise and Dan’l Boone does

d.

neither advertises

e.

can’t tell

b.

both advertise

Exhibit 10-15 depicts the payoff matrix facing Eagle Tobacco and Dan’l Boone Tobacco with respect to their decisions to advertise or not. Eagle Tobacco has a dominant strategy.

a.

True

b.

False

a. true

Exhibit 10-15 depicts the payoff matrix facing Eagle Tobacco and Dan’l Boone Tobacco with respect to their decisions to advertise or not. Eagle Tobacco’s dominant strategy is not to advertise.

a.

True

b.

False

b. false

Exhibit 10-15 depicts the payoff matrix facing Eagle Tobacco and Dan’l Boone Tobacco with respect to their decisions to advertise or not. Eagle Tobacco and Dan’l Boone Tobacco have the same dominant strategy.

a.

True

b.

False

a. true