front 5 John moved his office from a building he was renting downtown to the

carriage house he owns in back of his house. How will his costs change?

- explicit and implicit

costs rise

- explicit costs rise; implicit costs fall

- explicit and implicit costs fall

- explicit costs fall;

implicit costs rise

- not enough information is given

| |

front 6 A young chef is considering opening his own sushi bar. To do so, he

would have to quit his current job, which pays $20,000 a year, and

take over a store building that he owns and currently rents to his

brother for $6,000 a year. His expenses at the sushi bar would be

$50,000 for food and $2,000 for gas and electricity. What are his

explicit costs?

- $26,000

- $66,000

- $78,000

- $52,000

- $72,000

| |

front 7 A young chef is considering opening his own sushi bar. To do so, he

would have to quit his current job, which pays $20,000 a year, and

take over a store building that he owns and currently rents to his

brother for $6,000 a year. His expenses at the sushi bar would be

$50,000 for food and $2,000 for gas and electricity. What are his

implicit costs?

- $26,000

- $66,000

- $78,000

- $52,000

- $72,000

| |

front 8 Economic profit is defined as

- total revenue minus

implicit costs

- total revenue plus explicit costs

- total revenue plus implicit costs

- wages plus interest

minus rent

- total revenue minus implicit and explicit

costs

| |

front 9 Which of the following would be shown on IBM's accounting statement?

- revenue, implicit costs,

explicit costs, and economic profit

- revenue, implicit

costs, explicit costs, and accounting profit

- revenue,

explicit costs, and economic profit

- revenue, explicit

costs, and accounting profit

- revenue, implicit costs, and

accounting profit

| |

front 10 Sally owns a small business that she operates in a small building she

owns. Given the information in Exhibit 7-1, Sally's accounting profit is

- $80,000

- $50,000

- $65,000

- $35,000

- $24,000

| |

front 11 Sally owns a small business that she operates in a small building she

owns. Given the information in Exhibit 7-1, Sally's economic profit is

- $80,000

- $50,000

- $65,000

- $35,000

- $24,000

| |

front 12 Inputs that can be increased or decreased in the short run are called

- fixed inputs

- variable inputs

- economic inputs

- accounting

inputs

- normal inputs

| |

front 13 The short run is a period of time

- equal to or less than

six months

- during which all resources may be varied

- during which all resources are fixed

- during which at

least one resource is fixed

- during which at least one

resource may be varied

| |

front 14 Which of the following is most likely to be a fixed resource for the

Speedy Word Processing and Résumé Company?

- floppy disks

- typists

- computer terminals

- electricity

- paper

| |

front 15 The long run is a period of time

- during which at least

one resource is fixed

- during which all resources are

variable

- during which all resources are fixed

- less

than one year

- greater than one year

| |

front 16 Marginal product is defined as

- the increase in revenue

that occurs when an additional unit of a resource is added

- the increase in output that occurs when all resources are

increased by the same proportion

- the increase in output

that occurs when an additional unit of a resource is added, holding

all other resources constant

- the amount of additional

resources needed to increase output by one unit when all resources

are increased by the same amount

- the amount of additional

money needed to increase output by one unit when all resources are

held constant

| |

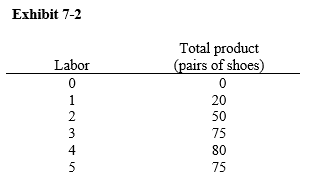

front 17 Given the information in Exhibit 7-2, what is the marginal product of

the third unit of labor?

- 45 pairs of shoes

- 25 pairs of shoes

- 15 pairs of shoes

- $45

- $25

| |

front 18 Given the information in Exhibit 7-2, at what point do diminishing

marginal returns set in?

- before the first unit of

labor

- between the first and second units of labor

- between the second and third units of labor

- between the

third and fourth units of labor

- between the fourth and

fifth units of labor

| |

front 19 Increasing marginal returns are generally the result of

- diseconomies of

scale

- increasing costs

- specialization and division

of labor

- labor unions

- technology

| |

front 20 If a firm is experiencing diminishing marginal returns to labor,

which of the following must be true?

- The first workers the

firm hired were better than the workers hired later on.

- The

firm is experiencing decreasing returns to scale.

- The

positive effect of specialization in production is being offset by

the negative effect of crowding of inputs.

- Output is

decreasing.

- The firm should buy more nonlabor inputs.

| |

front 21 The law of diminishing marginal returns states that

- long-run average cost

declines as output increases

- if the marginal product is

above the average product, the average will rise

- as units

of a variable input are added to a given amount of fixed inputs, the

marginal product of the variable input eventually diminishes

- as a person consumes more of a good, the marginal satisfaction

from that good eventually diminishes

- if marginal product is

positive, total product rises

| |

front 22 When diminishing marginal returns set in, total product

- is negative

- decreases at an increasing rate

- decreases at a

decreasing rate

- increases at an increasing rate

- increases at a decreasing rate

| |

front 23 Which of the following is most likely to be a fixed cost for any firm?

- the monthly electric

bill

- sales taxes

- shipping and postage costs

- rent on office space

- charitable donations

| |

front 24 A variable cost is one that changes

- in the long run

only

- in the short run only

- year to year

- month to month

- as output changes

| |

front 25 For a person who owns and operates an automobile, insurance premiums

are a __________ and maintenance and repairs are a __________.

- revenue; cost

- fixed cost; fixed cost

- variable cost; variable

cost

- variable cost; fixed cost

- fixed cost; variable

cost

| |

front 26 Fixed costs are defined as

- the total costs of a

firm's production

- the additional cost of the last unit

produced

- costs that increase proportionately as the quantity

produced increases

- costs that do not vary as quantity

produced increases

- implicit costs only

| |

front 27 What is true of marginal cost when marginal returns are increasing?

- It is zero.

- It

is negative.

- It is increasing.

- It is

decreasing.

- It has a constant slope.

| |

front 28 What is true of marginal cost when marginal returns are decreasing?

- It is zero.

- It

is negative.

- It is increasing.

- It is

decreasing.

- It has a constant slope.

| |

front 29 What is the relationship between marginal cost and marginal product?

- The two are not

related.

- When marginal product increases, marginal cost

increases.

- When marginal product increases, marginal cost

falls.

- When marginal product is negative, marginal costs are

negative.

- When diminishing marginal returns set in, marginal

costs fall.

| |

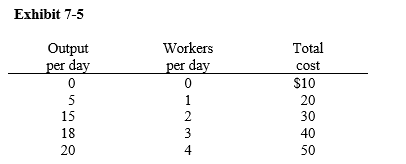

front 30 In Exhibit 7-5, what is fixed cost at 20 units of output?

- $0

- $10

- $40

- it is impossible to calculate fixed cost unless we

know the daily wage

- it is impossible to calculate fixed

cost unless we know variable cost at Q = 15

| |

front 31 In Exhibit 7-5, what is variable cost when no output is being produced?

- $0

- $10

- infinity

- it is impossible to calculate variable cost

unless we know the daily wage

- it is impossible to calculate

variable cost unless we know fixed cost at Q = 0

| |

front 32 In Exhibit 7-5, what are variable costs at 15 units of output?

- $30

- $10

- $1

- $20

- it is impossible to calculate variable

cost unless we know the daily wage

| |

front 33 In Exhibit 7-5, what is the marginal cost of the 15th unit of output

- $30

- $10

- $1

- $20

- it is impossible to calculate marginal

cost unless we know the daily wage

| |

front 34 When marginal product is decreasing, marginal cost is

- less than zero

- equal to zero

- constant

- decreasing

- increasing

| |

front 35 The average total cost curve and the average variable cost curve

- are closer together as

output increases, with average variable cost reaching its minimum

level first

- are closer together as output increases, with

average total cost reaching its minimum level first

- are

farther apart as output increases, with average variable cost

reaching its minimum level first

- are farther apart as

output increases, with average total cost reaching its minimum level

first

- are parallel to each other, and reach their minimum

levels at the same rate of output

| |

front 36 If the average height in the classroom were 5 feet 10 inches and

Patrick Ewing, who is 7 feet tall, came in and sat down,

- the average height would

rise to 7 feet

- the marginal height would be 5 feet 10

inches

- the average height would not change

- the

average height would rise somewhat

- the marginal height

would rise

| |

front 37 Which of the following correctly describes the relationship between

the marginal cost and average variable cost curves?

- MC is everywhere above

AVC

- AVC is everywhere above MC

- MC crosses AVC at

AVC's minimum point

- MC crosses AVC at MC's minimum

point

- both AVC and MC first rise and then fall

| |

front 38 If marginal cost exceeds average variable cost,

- average variable cost is

negative

- average variable cost is increasing

- marginal cost is greater than average total cost

- average variable cost is decreasing

- average fixed cost

is increasing

| |

front 39 If marginal cost is less than average total cost,

- marginal cost must be

falling

- average total cost must be increasing

- average variable cost equals average total cost

- average

variable cost must be decreasing

- average variable cost may

be increasing or decreasing

| |

front 40 Which of the following is true of the MC curve?

- It intersects the ATC

curve at its minimum, but it does not intersect the AVC curve at its

minimum.

- It intersects the AVC curve at its minimum, but it

does not intersect the ATC curve at its minimum.

- It

intersects both the ATC and the AVC curves at their minimums.

- It intersects both the ATC and the AFC curves at their

minimums.

- It intersects both the AVC and the AFC curves at

their minimums.

| |

front 41 The marginal cost curve intersects the average total cost curve (ATC)

- at the ATC's minimum

point

- only when the ATC is sloping upward

- at the

ATC's maximum point

- only when the ATC is sloping

downward

- when the ATC intersects the fixed cost curve

| |

front 42 The shape of the long-run average cost curve reflects

- market demand

- economies and diseconomies of scale

- increasing and

diminishing marginal returns

- productivity of fixed

inputs

- all of the above

| |

front 43 Economies of scale occur where

- long-run average cost

falls as new firms enter the industry

- short-run average

cost falls as new firms enter the industry

- long-run average

cost falls as one firm expands plant size

- short-run average

cost falls as one firm expands plant size

- long-run average

cost rises as one firm expands plant size

| |

front 44 Which economic concept explains why a large drugstore chain can

produce at a lower average cost than Whoville Pharmacy, an

individually owned drugstore?

- increasing marginal

returns

- diminishing marginal returns

- economies of

scale

- diseconomies of scale

- constant returns to

scale

| |

front 45 Doubling the circumference of an oil pipeline more than doubles the

volume of oil that can be pumped through. This is an example of

- production

inefficiency

- diminishing marginal returns

- diseconomies of scale

- constant returns to scale

- economies of scale

| |

front 46 For building contractors, doubling the size of an office building

does not require double the inputs because there are common walls.

This is an example of

- increasing marginal

product

- diminishing marginal returns

- economies of

scale

- diseconomies of scale

- constant returns to

scale

| |

front 47 The minimum efficient scale for a firm is the

- lowest rate of output at

which long-run average cost is at a minimum

- lowest rate of

output at which short-run average total cost is at a minimum

- lowest rate of output at which short-run average variable cost

is at a minimum

- average of the rates of output at which

long-run average cost is at a minimum

- average of the rates

of output at which short-run average total cost is at a minimum

| |

front 48 If General Electric finds that when it doubles both its plant size

and the amount of associated inputs, its output level does not double, then

- the law of diminishing

returns is in effect

- long-run average costs must be

decreasing

- the firm is experiencing diseconomies of

scale

- the firm should increase production

- the firm

is experiencing constant returns to scale

| |

front 49 As output increases, diseconomies of scale

- lead to rising long-run

average costs

- lead to declining long-run average costs

- lead to rising short-run average total costs

- lead to

declining short-run total cost

- means the law of diminishing

marginal returns is affecting production

| |