The risk structure of interest rates is

- A) the structure of how interest rates move over time.

- B) the relationship among interest rates of different bonds with the same maturity.

- C) the relationship among the term to maturity of different bonds.

- D) the relationship among interest rates on bonds with different maturities.

Answer: B

The risk that interest payments will not be made, or that the face value of a bond is not repaid when a bond matures is

- A) interest rate risk.

- B) inflation risk.

- C) liquidity risk.

- D) default risk.

Answer: D

Bonds with no default risk are called

- A) flower bonds.

- B) no-risk bonds.

- C) default-free bonds.

- D) zero-risk bonds.

Answer: C

Which of the following bonds are considered to be default-risk free?

- A) municipal bonds

- B) investment-grade bonds

- C) U.S. Treasury bonds

- D) junk bonds

Answer: C

U.S. government bonds have no default risk because

- A) they are issued in strictly limited quantities.

- B) the federal government can increase taxes or print money to pay its obligations.

- C) they are backed with gold reserves.

- D) they can be exchanged for silver at any time.

Answer: B

The spread between the interest rates on bonds with default risk and default-free bonds is called the

- A) risk premium.

- B) junk margin.

- C) bond margin.

- D) default premium.

Answer: A

If the probability of a bond default increases because corporations begin to suffer large losses, then the default risk on corporate bonds will ________ and the expected return on these bonds will ________, everything else held constant.

- A) decrease; increase

- B) decrease; decrease

- C) increase; increase

- D) increase; decrease

Answer: D

A bond with default risk will always have a ________ risk premium and an increase in its default risk will ________ the risk premium.

- A) positive; raise

- B) positive; lower

- C) negative; raise

- D) negative; lower

Answer: A

If a corporation begins to suffer large losses, then the default risk on the corporate bond will

- A) increase and the bond's return will become more uncertain, meaning the expected return on the corporate bond will fall.

- B) increase and the bond's return will become less uncertain, meaning the expected return on the corporate bond will fall.

- C) decrease and the bond's return will become less uncertain, meaning the expected return on the corporate bond will fall.

- D) decrease and the bond's return will become less uncertain, meaning the expected return on the corporate bond will rise.

Answer: A

If the possibility of a default increases because corporations begin to suffer losses, then the default risk on corporate bonds will ________, and the bonds' returns will become ________ uncertain, meaning that the expected return on these bonds will decrease, everything else held constant.

- A) increase; less

- B) increase; more

- C) decrease; less

- D) decrease; more

Answer: B

Other things being equal, an increase in the default risk of corporate bonds shifts the demand curve for corporate bonds to the ________ and the demand curve for Treasury bonds to the ________.

- A) right; right

- B) right; left

- C) left; right

- D) left; left

Answer: C

Other things being equal, a decrease in the default risk of corporate bonds shifts the demand curve for corporate bonds to the ________ and the demand curve for Treasury bonds to the ________.

- A) right; right

- B) right; left

- C) left; right

- D) left; left

Answer: B

A(n) ________ in the riskiness of corporate bonds will ________ the price of corporate bonds and ________ the yield on corporate bonds, all else equal.

- A) increase; increase; increase

- B) increase; decrease; increase

- C) decrease; increase; increase

- D) decrease; decrease;decrease

Answer: B

An increase in the riskiness of corporate bonds will ________ the price of corporate bonds and ________ the price of Treasury bonds, everything else held constant.

- A) increase; increase

- B) reduce; reduce

- C) reduce; increase

- D) increase; reduce

Answer: C

A decrease in the riskiness of corporate bonds will ________ the price of corporate bonds and ________ the price of Treasury bonds, everything else held constant.

- A) increase; increase

- B) reduce; reduce

- C) reduce; increase

- D) increase; reduce

Answer: D

An increase in the riskiness of corporate bonds will ________ the yield on corporate bonds and ________ the yield on Treasury securities, everything else held constant.

- A) increase; increase

- B) reduce; reduce

- C) increase; reduce

- D) reduce; increase

Answer: C

A decrease in the riskiness of corporate bonds will ________ the yield on corporate bonds and ________ the yield on Treasury securities, everything else held constant.

- A) increase; increase

- B) decrease; decrease

- C) increase; decrease

- D) decrease; increase

Answer: D

An increase in default risk on corporate bonds ________ the demand for these bonds, but ________ the demand for default-free bonds, everything else held constant.

- A) increases; lowers

- B) lowers; increases

- C) does not change; greatly increases

- D) moderately lowers; does not change

Answer: B

A decrease in default risk on corporate bonds ________ the demand for these bonds, and ________ the demand for default-free bonds, everything else held constant.

- A) increases; lowers

- B) lowers; increases

- C) does not change; greatly increases

- D) moderately lowers; does not change

Answer: A

As default risk increases, the expected return on corporate bonds ________, and the return becomes ________ uncertain, everything else held constant.

- A) increases; less

- B) increases; more

- C) decreases; less

- D) decreases; more

Answer: D

As default risk decreases, the expected return on corporate bonds ________, and the return becomes ________ uncertain, everything else held constant.

- A) increases; less

- B) increases; more

- C) decreases; less

- D) decreases; more

Answer: A

As their relative riskiness ________, the expected return on corporate bonds ________ relative to the expected return on default-free bonds, everything else held constant.

- A) increases; increases

- B) increases; decreases

- C) decreases; decreases

- D) decreases; does not change

Answer: B

Which of the following statements are TRUE?

- A) A decrease in default risk on corporate bonds lowers the demand for these bonds, but increases the demand for default-free bonds.

- B) The expected return on corporate bonds decreases as default risk increases.

- C) A corporate bond's return becomes less uncertain as default risk increases.

- D) As their relative riskiness increases, the expected return on corporate bonds increases relative to the expected return on default-free bonds.

Answer: B

Everything else held constant, if the federal government were to guarantee today that it will pay creditors if a corporation goes bankrupt in the future, the interest rate on corporate bonds will ________ and the interest rate on Treasury securities will ________.

- A) increase; increase

- B) increase; decrease

- C) decrease; increase

- D) decrease; decrease

Answer: C

Bonds with relatively high risk of default are called

- A) Brady bonds.

- B) junk bonds.

- C) zero coupon bonds.

- D) investment grade bonds.

Answer: B

Junk bonds, bonds with a low bond rating, are also known as

- A) high-yield bonds.

- B) investment grade bonds.

- C) high quality bonds.

- D) zero-coupon bonds.

Answer: A

Bonds with relatively low risk of default are called ________ securities and have a rating of Baa (or BBB) and above; bonds with ratings below Baa (or BBB) have a higher default risk and are called ________.

- A) investment grade; lower grade

- B) investment grade; junk bonds

- C) high quality; lower grade

- D) high quality; junk bonds

Answer: B

Which of the following bonds would have the highest default risk?

- A) municipal bonds

- B) investment-grade bonds

- C) U.S. Treasury bonds

- D) junk bonds

Answer: D

Which of the following long-term bonds has the highest interest rate?

- A) corporate Baa bonds

- B) U.S. Treasury bonds

- C) corporate Aaa bonds

- D) municipal bonds

Answer: A

Which of the following securities has the lowest interest rate?

- A) junk bonds

- B) U.S. Treasury bonds

- C) investment-grade bonds

- D) corporate Baa bonds

Answer: B

The spread between interest rates on low quality corporate bonds and U.S. government bonds

- A) widened significantly during the Great Depression.

- B) narrowed significantly during the Great Depression.

- C) narrowed moderately during the Great Depression.

- D) did not change during the Great Depression.

Answer: A

During the Great Depression years 1930-1933 there was a very high rate of business failures and defaults, we would expect the risk premium for ________ bonds to be very high.

- A) U.S. Treasury

- B) corporate Aaa

- C) municipal

- D) corporate Baa

Answer: D

Risk premiums on corporate bonds tend to ________ during business cycle expansions and ________ during recessions, everything else held constant.

- A) increase; increase

- B) increase; decrease

- C) decrease; increase

- D) decrease; decrease

Answer: C

The collapse of the subprime mortgage market

- A) did not affect the corporate bond market.

- B) increased the perceived riskiness of Treasury securities.

- C) reduced the Baa-Aaa spread.

- D) increased the Baa-Aaa spread.

Answer: D

The collapse of the subprime mortgage market increased the spread between Baa and default-free U.S. Treasury bonds. This is due to

- A) a reduction in risk.

- B) a reduction in maturity.

- C) a flight to quality.

- D) a flight to liquidity.

Answer: C

During a "flight to quality"

- A) the spread between Treasury bonds and Baa bonds increases.

- B) the spread between Treasury bonds and Baa bonds decreases.

- C) the spread between Treasury bonds and Baa bonds is not affected.

- D) the change in the spread between Treasury bonds and Baa bonds cannot be predicted.

Answer: A

If you have a very low tolerance for risk, which of the following bonds would you be least likely to hold in your portfolio?

- A) a U.S. Treasury bond

- B) a municipal bond

- C) a corporate bond with a rating of Aaa

- D) a corporate bond with a rating of Baa

Answer: D

Which of the following statements is TRUE?

- A) A liquid asset is one that can be quickly and cheaply converted into cash.

- B) The demand for a bond declines when it becomes less liquid, decreasing the interest rate spread between it and relatively more liquid bonds.

- C) The differences in bond interest rates reflect differences in default risk only.

- D) The corporate bond market is the most liquid bond market.

Answer: A

Corporate bonds are not as liquid as government bonds because

- A) fewer corporate bonds for any one corporation are traded, making them more costly to sell.

- B) the corporate bond rating must be calculated each time they are traded.

- C) corporate bonds are not callable.

- D) corporate bonds cannot be resold.

Answer: A

When the Treasury bond market becomes more liquid, other things equal, the demand curve for corporate bonds shifts to the ________ and the demand curve for Treasury bonds shifts to the ________.

- A) right; right

- B) right; left

- C) left; right

- D) left; left

Answer: C

When the Treasury bond market becomes less liquid, other things equal, the demand curve for corporate bonds shifts to the ________ and the demand curve for Treasury bonds shifts to the ________.

- A) right; right

- B) right; left

- C) left; right

- D) left; left

Answer: B

A decrease in the liquidity of corporate bonds, other things being equal, shifts the demand curve for corporate bonds to the ________ and the demand curve for Treasury bonds shifts to the ________.

- A) right; right

- B) right; left

- C) left; left

- D) left; right

Answer: D

An increase in the liquidity of corporate bonds, other things being equal, shifts the demand curve for corporate bonds to the ________ and the demand curve for Treasury bonds shifts to the ________.

- A) right; right

- B) right; left

- C) left; left

- D) left; right

Answer: B

A(n) ________ in the liquidity of corporate bonds will ________ the price of corporate bonds and ________ the yield on corporate bonds, all else equal.

- A) increase; increase; decrease

- B) increase; decrease; decrease

- C) decrease; increase; increase

- D) decrease; decrease; decrease

Answer: A

An increase in the liquidity of corporate bonds will ________ the price of corporate bonds and ________ the yield of Treasury bonds, everything else held constant.

- A) increase; increase

- B) reduce; reduce

- C) increase; reduce

- D) reduce; increase

Answer: A

A decrease in the liquidity of corporate bonds will ________ the yield of corporate bonds and ________ the yield of Treasury bonds, everything else held constant.

- A) increase; increase

- B) decrease; decrease

- C) increase; decrease

- D) decrease; increase

Answer: C

The risk premium on corporate bonds reflects the fact that corporate bonds have a higher default risk and are ________ U.S. Treasury bonds.

- A) less liquid than

- B) less speculative than

- C) tax-exempt unlike

- D) lower-yielding than

Answer: A

Which of the following statements is TRUE?

- A) State and local governments cannot default on their bonds.

- B) Bonds issued by state and local governments are called municipal bonds.

- C) All government issued bonds—local, state, and federal—are federal income tax exempt.

- D) The coupon payment on municipal bonds is usually higher than the coupon payment on Treasury bonds.

Answer: B

Everything else held constant, if the tax-exempt status of municipal bonds were eliminated, then

- A) the interest rates on municipal bonds would still be less than the interest rate on Treasury bonds.

- B) the interest rate on municipal bonds would equal the rate on Treasury bonds.

- C) the interest rate on municipal bonds would exceed the rate on Treasury bonds.

- D) the interest rates on municipal, Treasury, and corporate bonds would all increase.

Answer: C

Municipal bonds have default risk, yet their interest rates are lower than the rates on default-free Treasury bonds. This suggests that

- A) the benefit from the tax-exempt status of municipal bonds is less than their default risk.

- B) the benefit from the tax-exempt status of municipal bonds equals their default risk.

- C) the benefit from the tax-exempt status of municipal bonds exceeds their default risk.

- D) Treasury bonds are not default-free.

Answer: C

Everything else held constant, an increase in marginal tax rates would likely have the effect of ________ the demand for municipal bonds, and ________ the demand for U.S. government bonds.

- A) increasing; increasing

- B) increasing; decreasing

- C) decreasing; increasing

- D) decreasing; decreasing

Answer: B

Everything else held constant, a decrease in marginal tax rates would likely have the effect of ________ the demand for municipal bonds, and ________ the demand for U.S. government bonds.

- A) increasing; increasing

- B) increasing; decreasing

- C) decreasing; increasing

- D) decreasing; decreasing

Answer: C

Everything else held constant, the interest rate on municipal bonds rises relative to the interest rate on Treasury securities when

- A) income tax rates are lowered.

- B) income tax rates are raised.

- C) municipal bonds become more widely traded.

- D) corporate bonds become riskier.

Answer: A

Everything else held constant, if income tax rates were lowered, then

- A) the interest rate on municipal bonds would fall.

- B) the interest rate on Treasury bonds would rise.

- C) the interest rate on municipal bonds would rise.

- D) the price of Treasury bonds would fall.

Answer: C

Everything else held constant, abolishing the individual income tax will

- A) increase the interest rate on corporate bonds.

- B) reduce the interest rate on municipal bonds.

- C) increase the interest rate on municipal bonds.

- D) increase the interest rate on Treasury bonds.

Answer: C

Which of the following statements are TRUE?

- A) An increase in tax rates will increase the demand for Treasury bonds, lowering their interest rates.

- B) Because the tax-exempt status of municipal bonds was of little benefit to bond holders when tax rates were low, they had higher interest rates than U.S. government bonds before World War II.

- C) Interest rates on municipal bonds will be higher than comparable bonds without the tax exemption.

- D) Because coupon payments on municipal bonds are exempt from federal income tax, the expected after-tax return on them will be higher for individuals in lower income tax brackets.

Answer: B

The Obama administration increased the tax on the top income tax bracket from 35% to 39%. Supply and demand analysis predicts the impact of this change was a ________ interest rate on municipal bonds and a ________ interest rate on Treasury bonds, all else the same.

- A) higher; lower

- B) lower; lower

- C) higher; higher

- D) lower; higher

Answer: D

Three factors explain the risk structure of interest rates

- A) liquidity, default risk, and the income tax treatment of a security.

- B) maturity, default risk, and the income tax treatment of a security.

- C) maturity, liquidity, and the income tax treatment of a security.

- D) maturity, default risk, and the liquidity of a security.

Answer: A

The spread between the interest rates on Baa corporate bonds and U.S. government bonds is very large during the Great Depression years 1930-1933. Explain this difference using the bond supply and demand analysis.

Answer: During the Great Depression many businesses failed. The default risk for the corporate bond increased compared to the default-free Treasury bond. The demand for corporate bonds decreased while the demand for Treasury bonds increased resulting in a larger risk premium.

If the federal government where to raise the income tax rates, would this have any impact on a state's cost of borrowing funds? Explain.

Answer: Yes, if the federal government raises income tax rates, demand for municipal bonds which are federal income tax exempt would increase. This would lower the interest rate on the municipal bonds thus lowering the cost to the state of borrowing funds.

The term structure of interest rates is

- A) the relationship among interest rates of different bonds with the same maturity.

- B) the structure of how interest rates move over time.

- C) the relationship among the term to maturity of different bonds.

- D) the relationship among interest rates on bonds with different maturities.

Answer: D

A plot of the interest rates on default-free government bonds with different terms to maturity is called

- A) a risk-structure curve.

- B) a default-free curve.

- C) a yield curve.

- D) an interest-rate curve.

Answer: C

Differences in ________ explain why interest rates on Treasury securities are not all the same.

- A) risk

- B) liquidity

- C) time to maturity

- D) tax characteristics

Answer: C

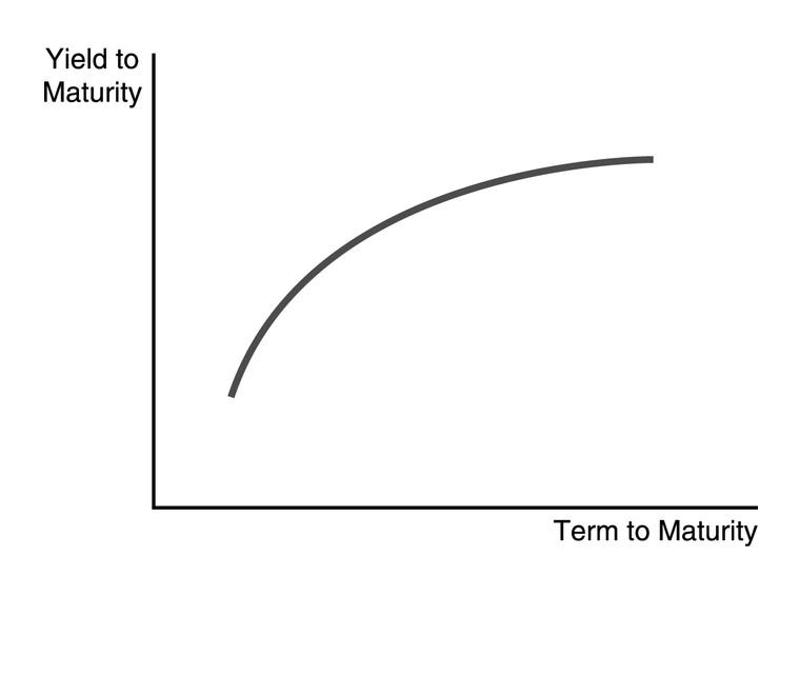

The typical shape for a yield curve is

- A) gently upward sloping.

- B) mound shaped.

- C) flat.

- D) bowl shaped.

Answer: A

When yield curves are steeply upward sloping

- A) long-term interest rates are above short-term interest rates.

- B) short-term interest rates are above long-term interest rates.

- C) short-term interest rates are about the same as long-term interest rates.

- D) medium-term interest rates are above both short-term and long-term interest rates.

Answer: A

When yield curves are flat

- A) long-term interest rates are above short-term interest rates.

- B) short-term interest rates are above long-term interest rates.

- C) short-term interest rates are about the same as long-term interest rates.

- D) medium-term interest rates are above both short-term and long-term interest rates.

Answer: C

When yield curves are downward sloping

- A) long-term interest rates are above short-term interest rates.

- B) short-term interest rates are above long-term interest rates.

- C) short-term interest rates are about the same as long-term interest rates.

- D) medium-term interest rates are above both short-term and long-term interest rates.

Answer: B

An inverted yield curve

- A) slopes up.

- B) is flat.

- C) slopes down.

- D) has a U shape.

Answer: C

Economists' attempts to explain the term structure of interest rates

- A) illustrate how economists modify theories to improve them when they are inconsistent with the empirical evidence.

- B) illustrate how economists continue to accept theories that fail to explain observed behavior of interest rate movements.

- C) prove that the real world is a special case that tends to get short shrift in theoretical models.

- D) have proved entirely unsatisfactory to date.

Answer: A

According to the expectations theory of the term structure, the interest rate on a long-term bond will equal the ________ of the short-term interest rates that people expect to occur over the life of the long-term bond.

- A) average

- B) sum

- C) difference

- D) multiple

Answer: A

If bonds with different maturities are perfect substitutes, then the ________ on these bonds must be equal.

- A) expected return

- B) surprise return

- C) surplus return

- D) excess return

Answer: A

If the expected path of one-year interest rates over the next five years is 4 percent, 5 percent, 7 percent, 8 percent, and 6 percent, then the expectations theory predicts that today's interest rate on the five-year bond is

- A) 4 percent.

- B) 5 percent.

- C) 6 percent.

- D) 7 percent.

Answer: C

If the expected path of 1-year interest rates over the next four years is 5 percent, 4 percent, 2 percent, and 1 percent, then the expectations theory predicts that today's interest rate on the four-year bond is

- A) 1 percent.

- B) 2 percent.

- C) 3 percent.

- D) 4 percent.

Answer: C

If the expected path of 1-year interest rates over the next five years is 1 percent, 2 percent, 3 percent, 4 percent, and 5 percent, the expectations theory predicts that the bond with the highest interest rate today is the one with a maturity of

- A) two years.

- B) three years.

- C) four years.

- D) five years.

Answer: D

If the expected path of 1-year interest rates over the next five years is 2 percent, 4 percent, 1 percent, 4 percent, and 3 percent, the expectations theory predicts that the bond with the lowest interest rate today is the one with a maturity of

- A) one year.

- B) two years.

- C) three years.

- D) four years.

Answer: A

Over the next three years, the expected path of 1-year interest rates is 4, 1, and 1 percent. The expectations theory of the term structure predicts that the current interest rate on 3-year bond is

- A) 1 percent.

- B) 2 percent.

- C) 3 percent.

- D) 4 percent.

Answer: B

According to the expectations theory of the term structure

- A) the interest rate on long-term bonds will exceed the average of short-term interest rates that people expect to occur over the life of the long-term bonds, because of their preference for short-term securities.

- B) interest rates on bonds of different maturities move together over time.

- C) buyers of bonds prefer short-term to long-term bonds.

- D) buyers require an additional incentive to hold long-term bonds.

Answer: B

According to the expectations theory of the term structure

- A) when the yield curve is steeply upward sloping, short-term interest rates are expected to remain relatively stable in the future.

- B) when the yield curve is downward sloping, short-term interest rates are expected to remain relatively stable in the future.

- C) investors have strong preferences for short-term relative to long-term bonds, explaining why yield curves typically slope upward.

- D) yield curves should be equally likely to slope downward as slope upward.

Answer: D

According to the segmented markets theory of the term structure

- A) bonds of one maturity are close substitutes for bonds of other maturities, therefore, interest rates on bonds of different maturities move together over time.

- B) the interest rate for each maturity bond is determined by supply and demand for that maturity bond.

- C) investors' strong preferences for short-term relative to long-term bonds explains why yield curves typically slope downward.

- D) because of the positive term premium, the yield curve will not be observed to be downward-sloping.

Answer: B

According to the segmented markets theory of the term structure

- A) the interest rate on long-term bonds will equal an average of short-term interest rates that people expect to occur over the life of the long-term bonds.

- B) buyers of bonds do not prefer bonds of one maturity over another.

- C) interest rates on bonds of different maturities do not move together over time.

- D) buyers require an additional incentive to hold long-term bonds.

Answer: C

A key assumption in the segmented markets theory is that bonds of different maturities

- A) are not substitutes at all.

- B) are perfect substitutes.

- C) are substitutes only if the investor is given a premium incentive.

- D) are substitutes but not perfect substitutes.

Answer: A

The segmented markets theory can explain

- A) why yield curves usually tend to slope upward.

- B) why interest rates on bonds of different maturities tend to move together.

- C) why yield curves tend to slope upward when short-term interest rates are low and to be inverted when short-term interest rates are high.

- D) why yield curves have been used to forecast business cycles.

Answer: A

According to the liquidity premium theory of the term structure

- A) because buyers of bonds may prefer bonds of one maturity over another, interest rates on bonds of different maturities do not move together over time.

- B) the interest rate on long-term bonds will equal an average of short-term interest rates that people expect to occur over the life of the long-term bonds plus a term premium.

- C) because of the positive term premium, the yield curve will not be observed to be downward sloping.

- D) the interest rate for each maturity bond is determined by supply and demand for that maturity bond.

Answer: B

According to the liquidity premium theory of the term structure

- A) bonds of different maturities are not substitutes.

- B) if yield curves are downward sloping, then short-term interest rates are expected to fall by so much that, even when the positive term premium is added, long-term rates fall below short-term rates.

- C) yield curves should never slope downward.

- D) interest rates on bonds of different maturities do not move together over time.

Answer: B

The additional incentive that the purchaser of a Treasury security requires to buy a long-term security rather than a short-term security is called the

- A) risk premium.

- B) term premium.

- C) tax premium.

- D) market premium.

Answer: B

If 1-year interest rates for the next three years are expected to be 1, 1, and 1 percent, and the 3-year term premium is 1 percent, than the 3-year bond rate will be

- A) 1 percent.

- B) 2 percent.

- C) 3 percent.

- D) 4 percent.

Answer: B

If 1-year interest rates for the next five years are expected to be 4, 2, 5, 4, and 5 percent, and the 5-year term premium is 1 percent, than the 5-year bond rate will be

- A) 2 percent.

- B) 3 percent.

- C) 4 percent.

- D) 5 percent.

Answer: D

According to the liquidity premium theory of the term structure, a steeply upward sloping yield curve indicates that short-term interest rates are expected to

- A) rise in the future.

- B) remain unchanged in the future.

- C) decline moderately in the future.

- D) decline sharply in the future.

Answer: A

According to the liquidity premium theory of the term structure, a slightly upward sloping yield curve indicates that short-term interest rates are expected to

- A) rise in the future.

- B) remain unchanged in the future.

- C) decline moderately in the future.

- D) decline sharply in the future.

Answer: B

According to the liquidity premium theory of the term structure, a flat yield curve indicates that short-term interest rates are expected to

- A) rise in the future.

- B) remain unchanged in the future.

- C) decline moderately in the future.

- D) decline sharply in the future.

Answer: C

According to the liquidity premium theory of the term structure, a downward sloping yield curve indicates that short-term interest rates are expected to

- A) rise in the future.

- B) remain unchanged in the future.

- C) decline moderately in the future.

- D) decline sharply in the future.

Answer: D

According to the liquidity premium theory, a yield curve that is flat means that

- A) bond purchasers expect interest rates to rise in the future.

- B) bond purchasers expect interest rates to stay the same.

- C) bond purchasers expect interest rates to fall in the future.

- D) the yield curve has nothing to do with expectations of bond purchasers.

Answer: C

If the yield curve is flat for short maturities and then slopes downward for longer maturities, the liquidity premium theory (assuming a mild preference for shorter-term bonds) indicates that the market is predicting

- A) a rise in short-term interest rates in the near future and a decline further out in the future.

- B) constant short-term interest rates in the near future and a decline further out in the future.

- C) a decline in short-term interest rates in the near future and a rise further out in the future.

- D) a decline in short-term interest rates in the near future and an even steeper decline further out in the future.

Answer: D

If the yield curve slope is flat for short maturities and then slopes steeply upward for longer maturities, the liquidity premium theory (assuming a mild preference for shorter-term bonds) indicates that the market is predicting

- A) a rise in short-term interest rates in the near future and a decline further out in the future.

- B) constant short-term interest rates in the near future and further out in the future.

- C) a decline in short-term interest rates in the near future and a rise further out in the future.

- D) constant short-term interest rates in the near future and a decline further out in the future.

Answer: C

If the yield curve has a mild upward slope, the liquidity premium theory (assuming a mild preference for shorter-term bonds) indicates that the market is predicting

- A) a rise in short-term interest rates in the near future and a decline further out in the future.

- B) constant short-term interest rates in the near future and further out in the future.

- C) a decline in short-term interest rates in the near future and a rise further out in the future.

- D) a decline in short-term interest rates in the near future and an even steeper decline further out in the future.

Answer: B

The preferred habitat theory of the term structure is closely related to the

- A) expectations theory of the term structure.

- B) segmented markets theory of the term structure.

- C) liquidity premium theory of the term structure.

- D) the inverted yield curve theory of the term structure.

Answer: C

The expectations theory and the segmented markets theory do not explain the facts very well, but they provide the groundwork for the most widely accepted theory of the term structure of interest rates

- A) the Keynesian theory.

- B) the separable markets theory.

- C) the liquidity premium theory.

- D) the asset market approach.

Answer: C

The ________ of the term structure of interest rates states that the interest rate on a long-term bond will equal the average of short-term interest rates that individuals expect to occur over the life of the long-term bond, and investors have no preference for short-term bonds relative to long-term bonds.

- A) segmented markets theory

- B) expectations theory

- C) liquidity premium theory

- D) separable markets theory

Answer: B

According to this theory of the term structure, bonds of different maturities are not substitutes for one another.

- A) segmented markets theory

- B) expectations theory

- C) liquidity premium theory

- D) separable markets theory

Answer: A

In actual practice, short-term interest rates and long-term interest rates usually move together; this is the major shortcoming of the

- A) segmented markets theory.

- B) expectations theory.

- C) liquidity premium theory.

- D) separable markets theory.

Answer: A

The ________ of the term structure states the following: the interest rate on a long-term bond will equal an average of short-term interest rates expected to occur over the life of the long-term bond plus a term premium that responds to supply and demand conditions for that bond.

- A) segmented markets theory

- B) expectations theory

- C) liquidity premium theory

- D) separable markets theory

Answer: C

A particularly attractive feature of the ________ is that it tells you what the market is predicting about future short-term interest rates by just looking at the slope of the yield curve.

- A) segmented markets theory

- B) expectations theory

- C) liquidity premium theory

- D) separable markets theory

Answer: C

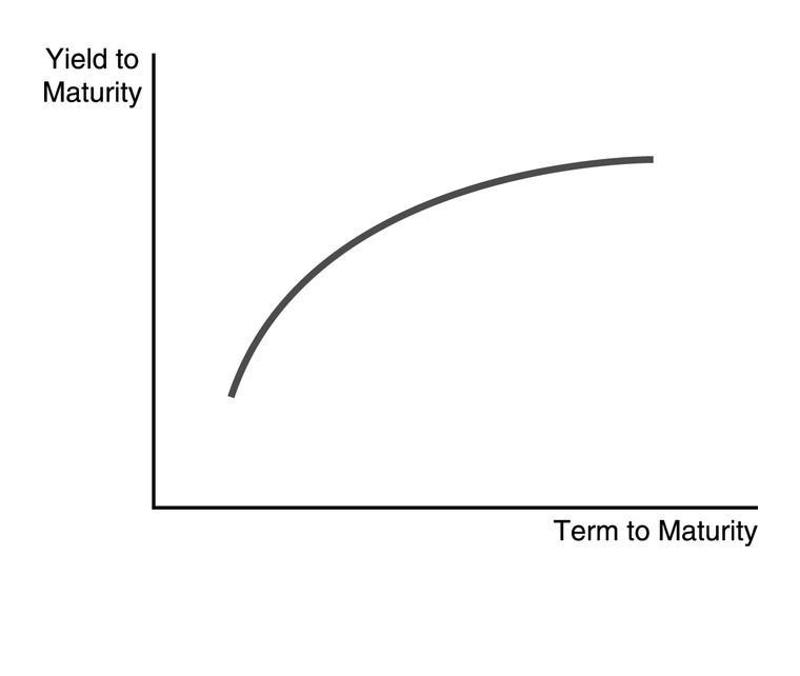

The steeply upward sloping yield curve in the figure above indicates that

- A) short-term interest rates are expected to rise in the future.

- B) short-term interest rates are expected to fall moderately in the future.

- C) short-term interest rates are expected to fall sharply in the future.

- D) short-term interest rates are expected to remain unchanged in the future.

Answer: A

The steeply upward sloping yield curve in the figure above indicates that ________ interest rates are expected to ________ in the future.

- A) short-term; rise

- B) short-term; fall moderately

- C) short-term; remain unchanged

- D) long-term; fall moderately

Answer: A

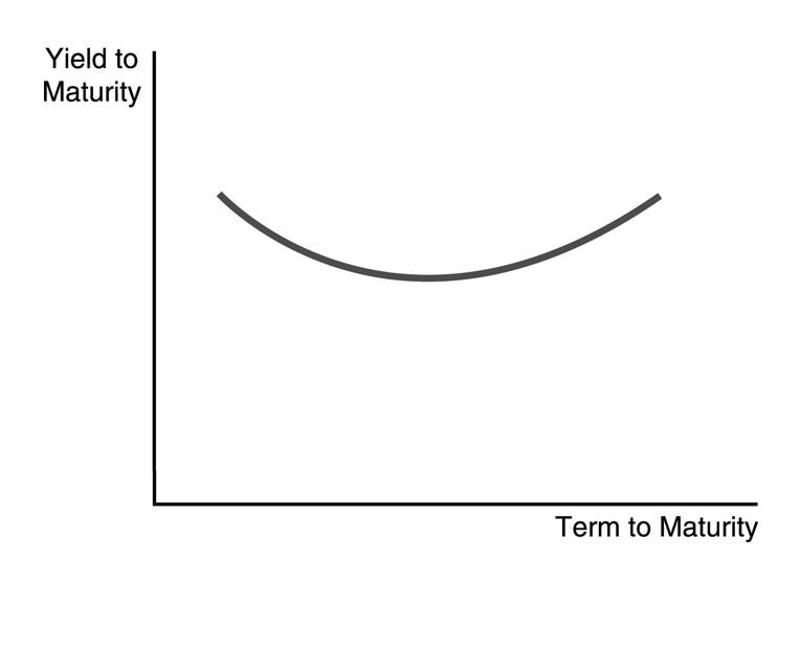

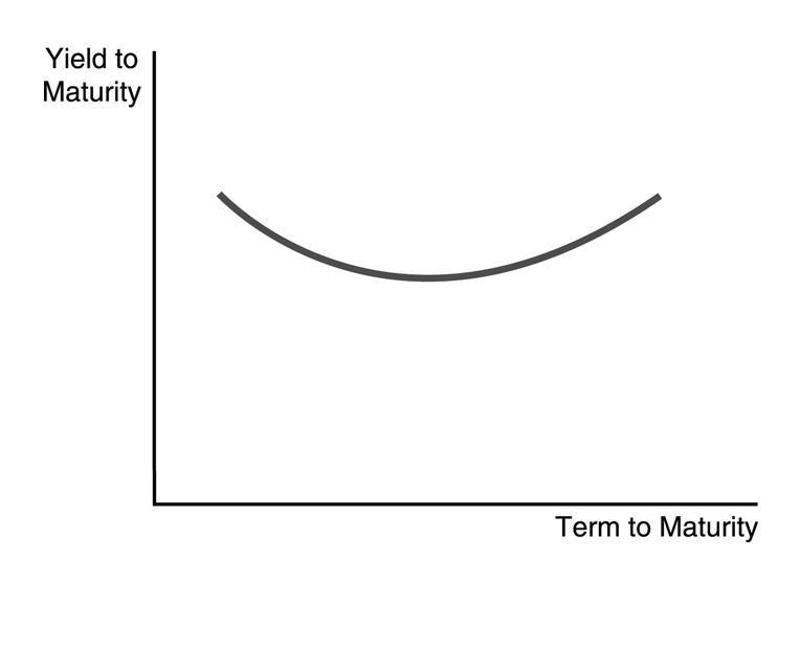

The U-shaped yield curve in the figure above indicates that short-term interest rates are expected to

- A) rise in the near-term and fall later on.

- B) fall sharply in the near-term and rise later on.

- C) fall moderately in the near-term and rise later on.

- D) remain unchanged in the near-term and rise later on.

Answer: B

The U-shaped yield curve in the figure above indicates that the inflation rate is expected to

- A) remain constant in the near-term and fall later on.

- B) fall sharply in the near-term and rise later on.

- C) rise moderately in the near-term and fall later on.

- D) remain constant in the near-term and rise later on.

Answer: B

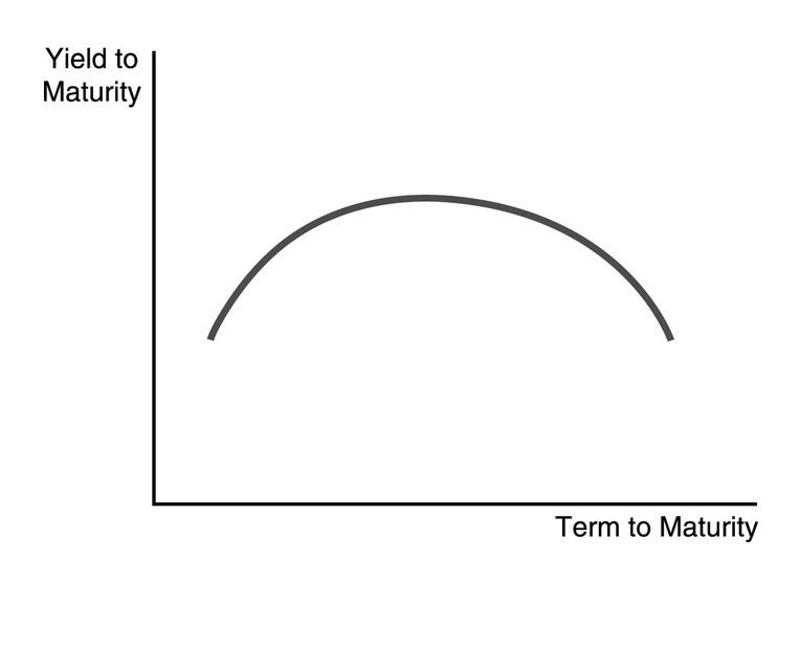

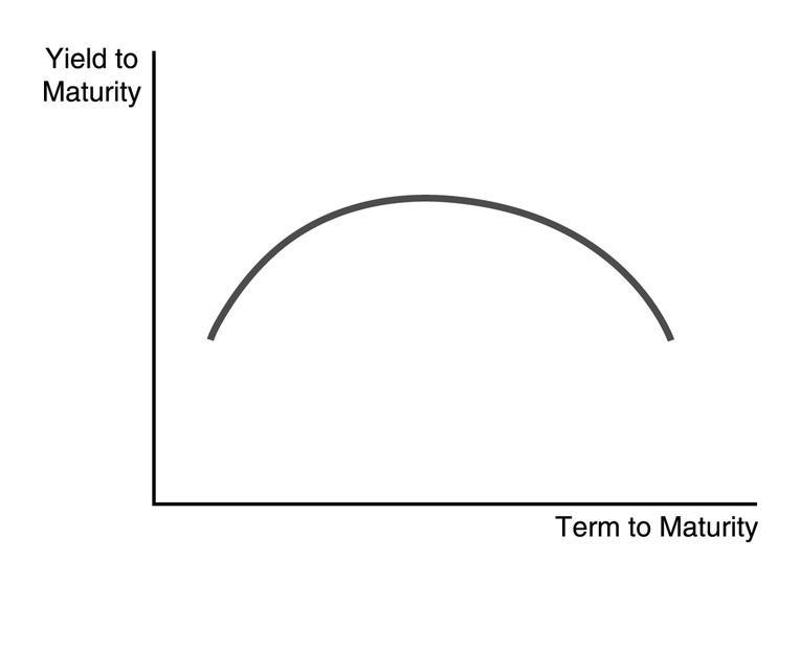

The mound-shaped yield curve in the figure above indicates that short-term interest rates are expected to

- A) rise in the near-term and fall later on.

- B) fall moderately in the near-term and rise later on.

- C) fall sharply in the near-term and rise later on.

- D) remain unchanged in the near-term and fall later on.

Answer: A

The mound-shaped yield curve in the figure above indicates that the inflation rate is expected to

- A) remain constant in the near-term and fall later on.

- B) fall moderately in the near-term and rise later on.

- C) rise moderately in the near-term and fall later on.

- D) remain unchanged in the near-term and rise later on.

Answer: C

An inverted yield curve predicts that short-term interest rates

- A) are expected to rise in the future.

- B) will rise and then fall in the future.

- C) will remain unchanged in the future.

- D) will fall in the future.

Answer: D

When short-term interest rates are expected to fall sharply in the future, the yield curve will

- A) slope up.

- B) be flat.

- C) be inverted.

- D) be an inverted U shape.

Answer: C

If investors expect interest rates to fall significantly in the future, the yield curve will be inverted. This means that the yield curve has a ________ slope.

- A) steep upward

- B) slight upward

- C) flat

- D) downward

Answer: D

When the yield curve is flat or downward-sloping, it suggest that the economy is more likely to enter

- A) a recession.

- B) an expansion.

- C) a boom time.

- D) a period of increasing output.

Answer: A

A ________ yield curve predicts a future increase in inflation.

- A) steeply upward sloping

- B) slight upward sloping

- C) flat

- D) downward sloping

Answer: A

If a higher inflation is expected, what would you expect to happen to the shape of the yield curve? Why?

Answer: The yield curve should have a steep upward slope. Nominal interest rates will increase if the inflation rate increases, therefore, bond purchasers will require a higher term premium to hold the riskier long-term bond.